This Wednesday, March 25, I will be in Madrid at Converge: Material Intelligence organized by PATIO Campus, speaking with industrial leaders about how artificial intelligence is reshaping the way companies design, use and recover materials. I think these conversations will echo the consistent message I’ve been hearing lately: Sustainability ambition is rising, but execution complexity is rising even faster.

The real challenge for the coming decade is not defining sustainability goals. It is aligning the digital foundations that make those goals achievable at scale. As we close in on 2030, the convergence between sustainability leadership and technology leadership is becoming one of the most decisive factors in industrial competitiveness.

From Parallel Agendas to Shared Enterprise Architecture

For many years, sustainability and digital transformation have evolved as parallel agendas. They’ve both evolved rapidly and they have both done so in the past decade. But those parallel agendas might be drifting closer together.

Chief Sustainability Officers (CSOs) focused on reporting, stakeholder expectations and regulatory readiness. Chief Information Officers (CIOs) concentrated on systems efficiency, integration and cybersecurity.

These are two clearly distinct business areas. So, what is behind this force of attraction between them?

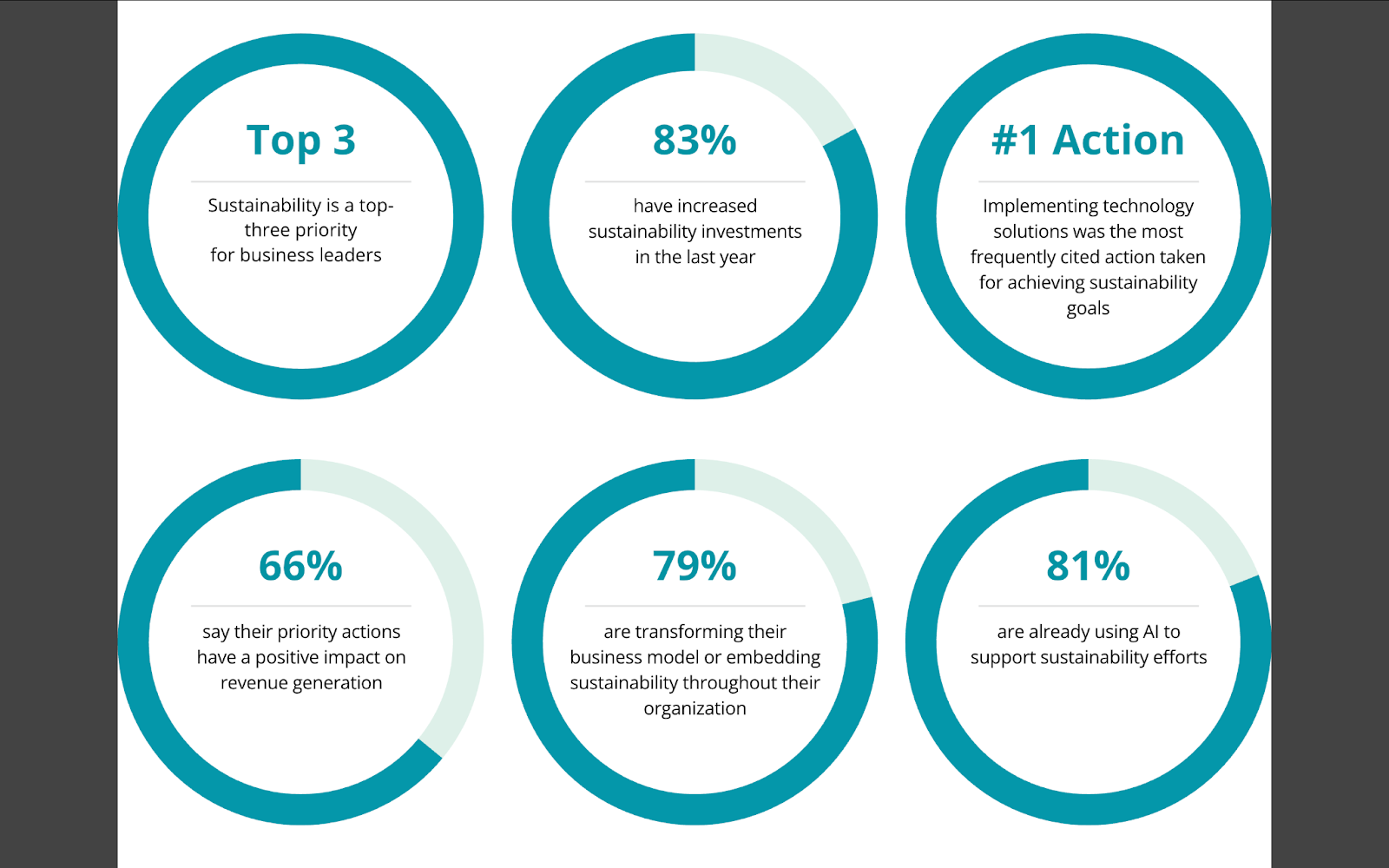

According to the latest Delloite Global C-suite Research, sustainability remains among the top strategic priorities for business leaders, with more than 80 percent of executives increasing related investments in the past year. At the same time, technology adoption and artificial intelligence are ranked among the most critical enablers for achieving sustainability goals. The implication is clear. Sustainability outcomes now depend directly on enterprise data architecture and decision intelligence capabilities.

In our own analysis at Finboot,we explored how transparency is now a capital allocation strategy.Transparency is no longer simply a reputational concern. It is becoming a financial variable that influences access to capital, risk exposure and long-term valuation. Companies able to demonstrate credible, data-driven sustainability performance are positioning themselves more strongly in increasingly volatile markets.

For CIOs, this elevates the data infrastructure they oversee into a core strategic company asset. For CSOs, it transforms sustainability from a compliance exercise into a cross-functional mandate with top line implications.

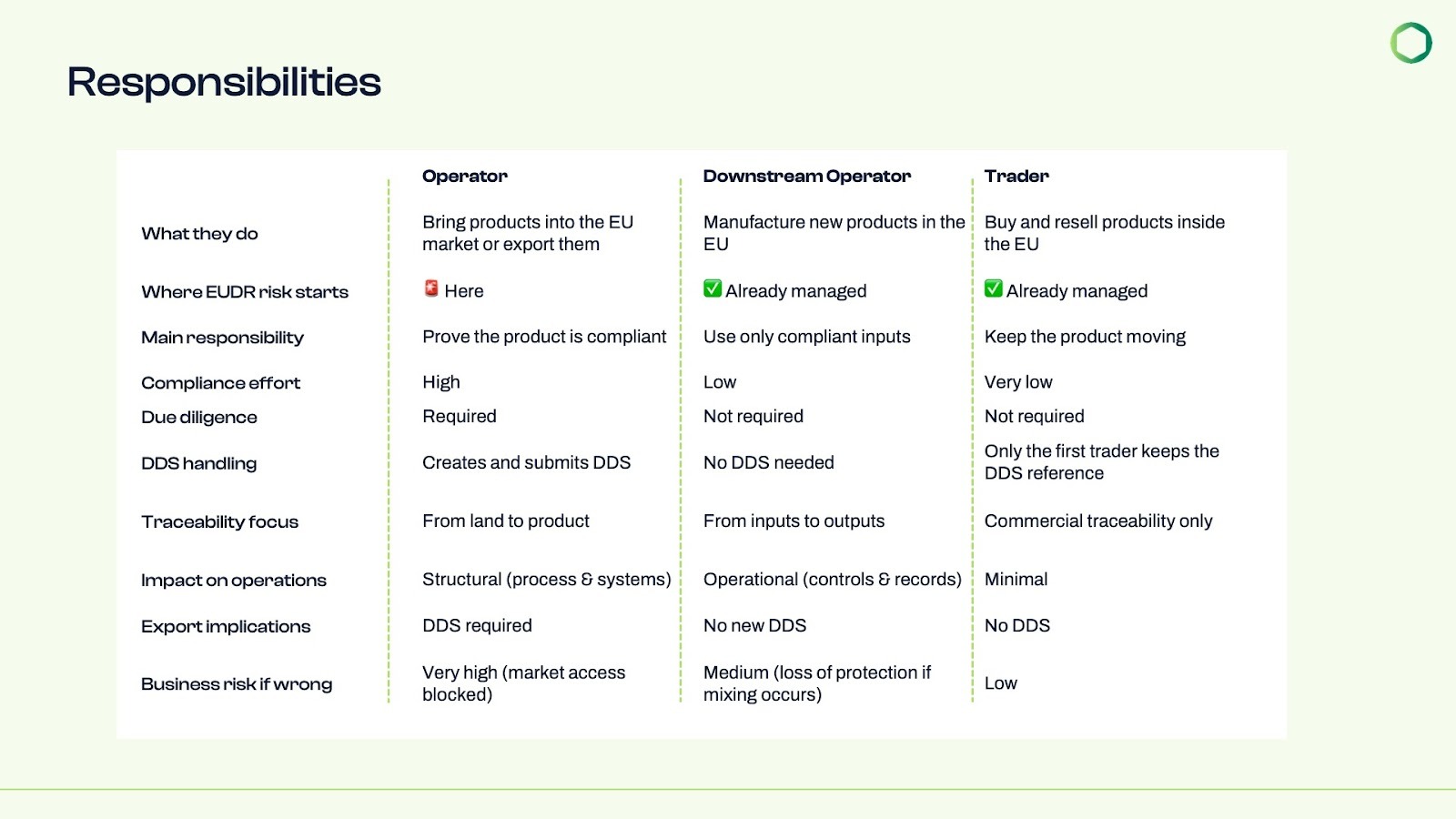

The Cost of Invisible Supply Chains

Despite rapid digital progress, many industrial supply chains remain structurally opaque. Material blending, multi-tier sourcing networks and fragmented reporting processes still limit the reliability of sustainability data.

This lack of visibility has tangible operational consequences. Recent industry research shows that around 60 percent of organisations consider limited supply chain transparency a major risk management challenge. Without trusted data on material origin, emissions profiles or supplier practices, companies face higher audit costs, slower decision cycles and increased exposure to regulatory disruption. In an environment shaped by geopolitical uncertainty, climate volatility and resource constraints, visibility is no longer optional.

Digital Traceability as an Enabler of Sustainability Goals

Leading industrial organisations are responding by investing in digital traceability systems that connect physical material flows with verified sustainability data. When implemented effectively, these capabilities move beyond compliance and begin to influence core business performance.

In the chemicals sector, for example, companies are deploying mass balance traceability models to verify the integration of sustainable feedstocks into complex production processes. This allows them to meet regulatory expectations while optimising procurement strategies and protecting margin structures.

In energy and advanced fuels, digital chain-of-custody solutions are being used to validate the origin and lifecycle emissions of renewable inputs. This reduces reporting friction and accelerates certification processes across global markets.

In manufacturing and packaging ecosystems, pilot programmes around Digital Product Passports are enabling product-level transparency on recyclability, material composition and environmental footprint. These initiatives are already influencing product design decisions and opening new opportunities for circular business models.

What we are seeing in practice is that traceability becomes a decision infrastructure. It allows organisations to move from retrospective sustainability reporting toward predictive operational optimisation. Advanced analytics and artificial intelligence are increasingly layered on top of this data foundation, helping companies anticipate disruptions, reduce waste and allocate resources more intelligently.

The Regulatory Push

While I still believe market dynamics will soon become the biggest driving force behind sustainability, it is undeniable that at present industrial transformation is strongly influenced by evolving regulatory frameworks. Initiatives such as the Corporate Sustainability Reporting Directive, the Ecodesign for Sustainable Products Regulation and the Carbon Border Adjustment Mechanism are already reshaping procurement models, product development strategies and supplier engagement processes.

These regulations do more than increase disclosure requirements. They are accelerating the need for integrated governance between sustainability, operations and digital teams. Compliance readiness increasingly depends on system architecture, data interoperability and real-time performance monitoring.

Executives are beginning to recognise that incremental adjustments will not be sufficient. Strategic redesign of processes, technology stacks and organisational collaboration models is becoming necessary to remain competitive.

For a deeper perspective on how regulatory transformation is shaping this evolution, executives can explore our Green Deal 2030 Executive Playbook.

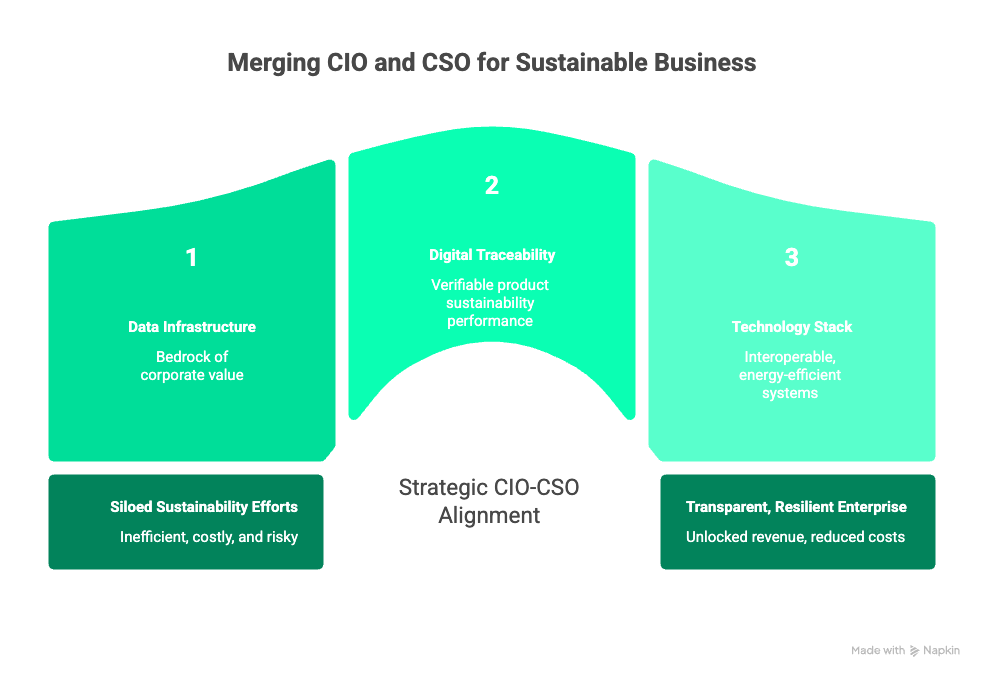

Building the Right Digital Sustainability Stack

To navigate this shift successfully, organisations are focusing on three interconnected priorities.

First, establishing trusted data infrastructure. Distributed ledger technologies and advanced verification systems are being adopted to create tamper-proof records of material provenance and chain of custody, particularly in sectors such as critical minerals, recycling and renewable energy.

Second, selecting traceability models that reflect operational reality. Identity preservation approaches may be appropriate for high-value materials, while mass balance frameworks often provide a pragmatic path for industries dealing with commingled inputs. Tools should be capable of combining different models into the same supply chains.

Third, ensuring interoperability across ecosystems. As supply chains become more collaborative and regulations more stringent, the ability for platforms to exchange data seamlessly will be essential to reduce onboarding friction and audit complexity.

Ultimately, the objective is not technological sophistication in isolation. It is combining tools and resources with the right formula to enable and accelerate business success.

A New Leadership Compass for 2030

The convergence of sustainability and digital transformation signals a broader evolution in C-suite leadership dynamics. Forward-looking companies are reframing sustainability as a driver of innovation, efficiency and long-term value creation rather than as a regulatory burden.

In my experience, the industrial leaders making the greatest progress are those willing to rethink traditional organisational boundaries. They are aligning CIO and CSO agendas around shared objectives, building digital capabilities that enable measurable environmental performance, and embedding sustainability considerations directly into operational strategy.

As industry discussions increasingly focus on themes such as material intelligence, AI-driven supply chain optimisation and circular value chains, one conclusion stands out. Strategic ambition alone will not determine competitive outcomes. Execution capability will. So, my recommendation:

Executive Next Steps:

Map Exposure: Quantify, if you haven’t yet, your exposure to regulations like CBAM and ESPR.

Pilot DPP: Start a Digital Product Passport pilot for your highest-risk product category.

Align Infrastructure: Transition from analog reporting to a blockchain-enabled "single source of truth".

This is why aligning sustainability vision with digital architecture is becoming one of the defining leadership challenges of the coming decade.

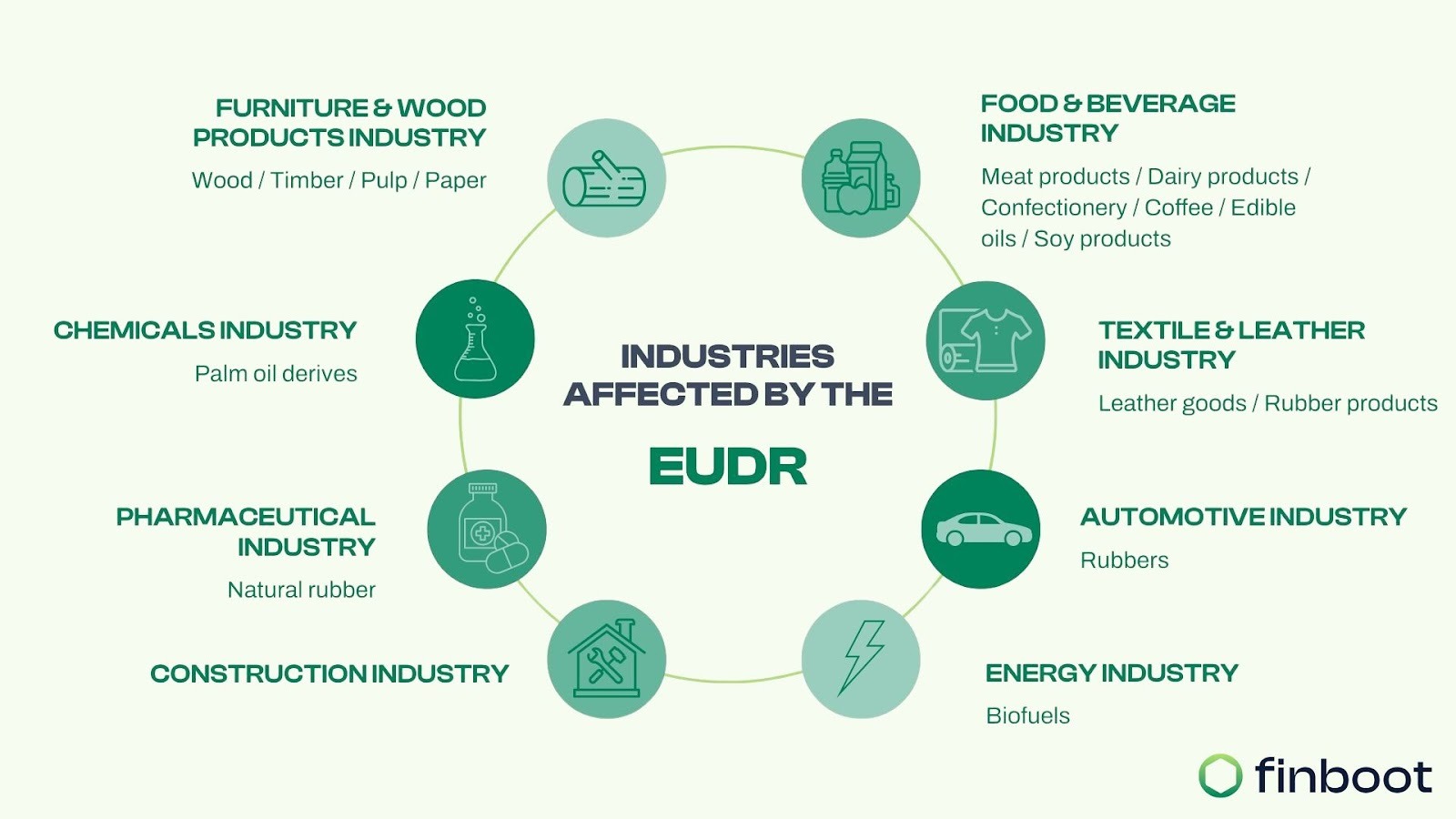

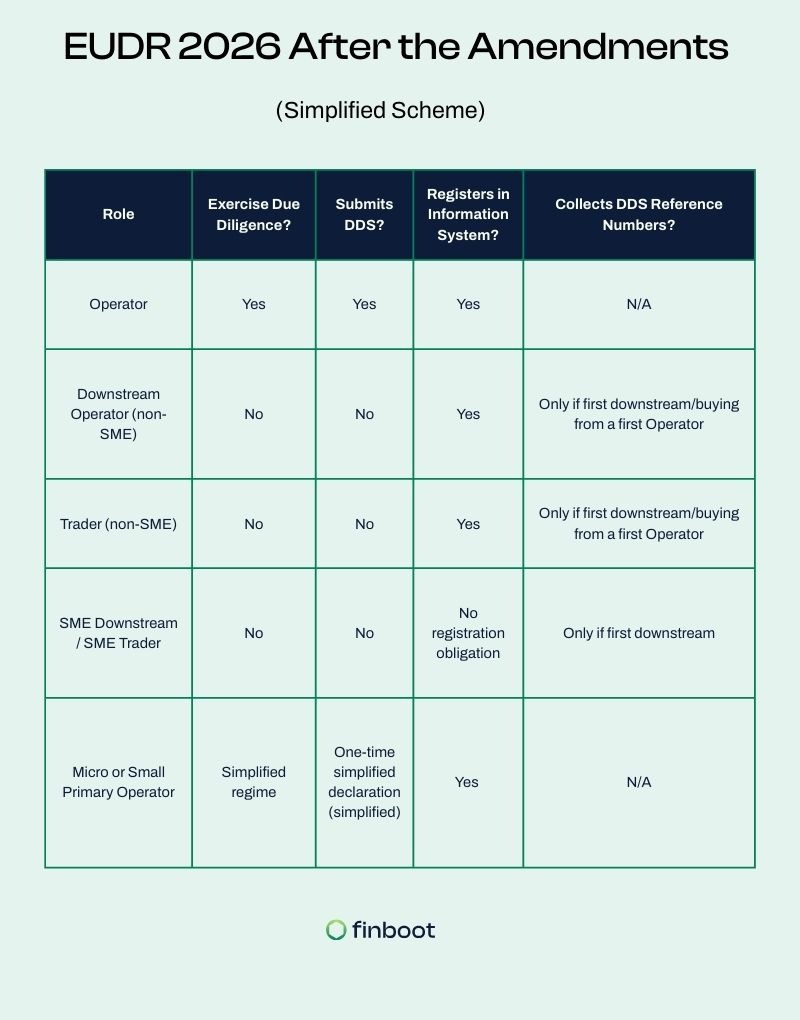

When Regulation (EU) 2025/2650 was adopted in December 2025, many organisations interpreted it as a regulatory softening of the EU Deforestation Regulation (EUDR). Legally, it introduces simplifications. Operationally, however, it introduces precision.

Over the past year, while supporting industrial leaders (including multinational chemical manufacturers navigating complex, multi-tier supply chains), I have seen how difficult it is to translate EUDR from legal language into executable process. The 2025 amendment does not dilute responsibility. It clarifies roles, redefines downstream obligations and places traceability systems at the centre of compliance.

For companies preparing for EUDR 2026, the question is no longer “Who submits a due diligence statement?” The question is whether their internal systems can structurally distinguish operators from downstream actors, manage declaration identifiers and reference numbers correctly, and withstand quantified enforcement thresholds.

Amended EUDR reshapes the operational logic of the Regulation. Understanding that shift now will determine whether implementation in 2026 is controlled — or reactive.

1. The Timeline Has Shifted, But the Pressure Has Not

Under Article 38 as amended :

The main obligations now apply from 30 December 2026

For operators that are natural persons or micro/small undertakings established as such by 31 December 2024, obligations apply from 30 June 2027

This 12-month postponement was introduced to allow businesses and IT systems to prepare.

But what I see in practice is different:

The regulatory bar hasn’t been lowered, It has simply given companies one more year to build infrastructure properly.

And infrastructure is the real issue.

2. The Most Important Structural Change: A New Supply Chain Category

The final text agreed by both Parliament and the Council on December 2025, formally introduces a new category:

“Downstream operator”

This matters enormously.

Previously, many companies assumed that every transformation restarted due diligence. That assumption is now clearly incorrect.

Below is a simplified representation of the updated structure under the amended Regulation:

The legal basis for this restructuring appears in the amended Articles 2, 4 and 5 .

What changed in substance?

Downstream operators and traders:

No longer submit due diligence statements

No longer “ascertain” due diligence in the previous way

Must collect and retain specific information

Must ensure traceability continuity

The obligation to collect DDS reference numbers applies only to the first downstream operator or trader

This is not cosmetic. It fundamentally reduces duplication in the Information System.

But it does not remove traceability obligations.

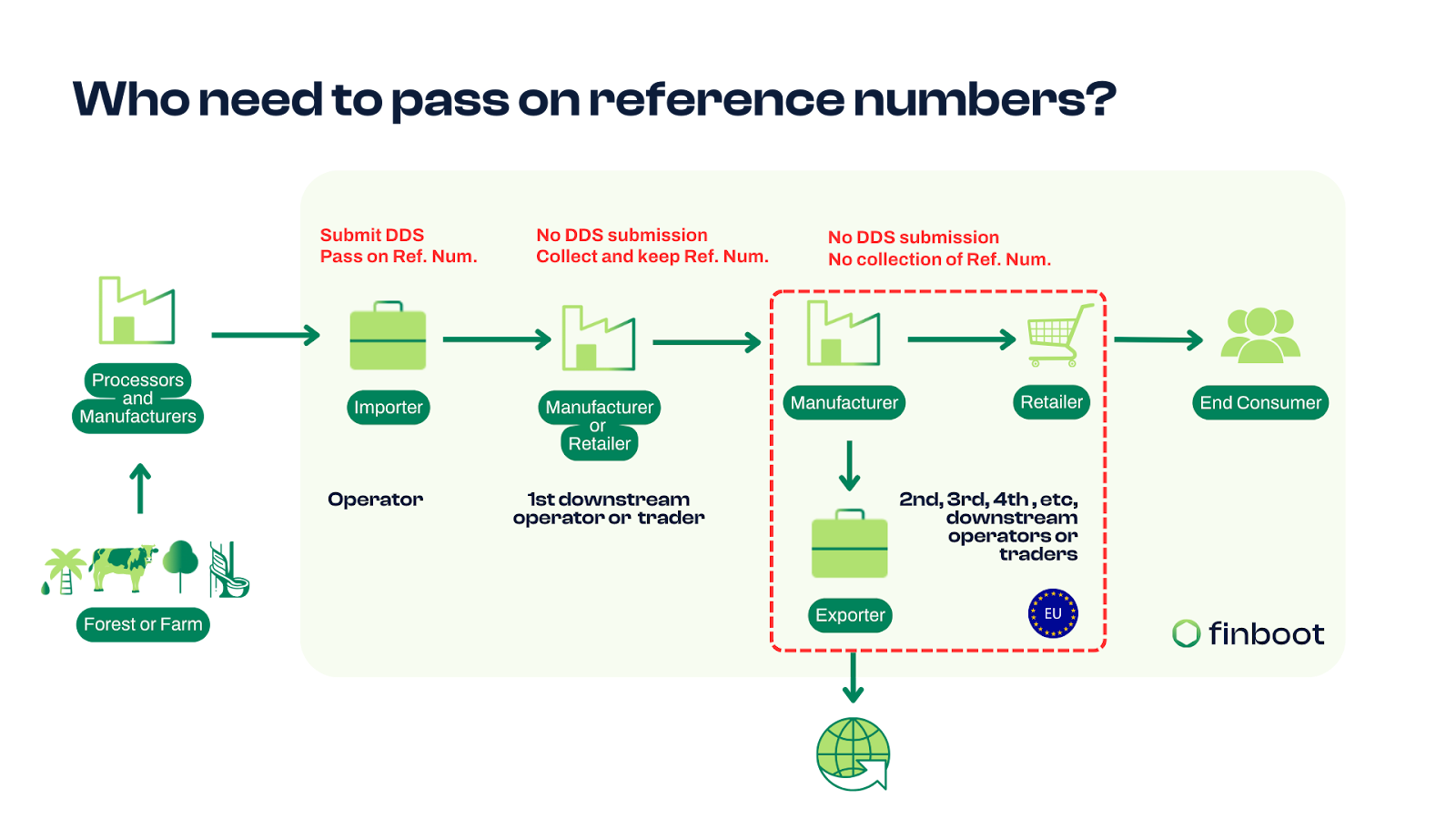

3. Reference Numbers: The Most Misunderstood Obligation

In nearly every EUDR workshop I lead, reference numbers become the moment of confusion.

To clarify this visually, below is the simplified logic we use internally to explain it to clients:

(Who needs to pass on reference numbers)

Under Article 4(7) and Article 5(3) as amended :

Operators must communicate DDS reference numbers (or declaration identifiers for micro/small primary operators) downstream.

The first downstream operator or trader must collect and retain those reference numbers.

Further downstream actors are not required to collect or verify DDS references.

The amendment explicitly limits this obligation to the first downstream actor to reduce system load .

However, and this is where implementation matters, companies must still ensure that the material they process is fully covered by a valid DDS or simplified declaration.

Here’s an example:

Downstream operators are, for example, a chocolate manufacturer using cocoa covered by a due diligence declaration, or a furniture manufacturer using timber covered by a simplified declaration. Downstream operators are not required to submit due diligence declarations; only operators who place products on the Union market for the first time (primary operators) are required to submit due diligence declarations.

In practice, that requires system-level linkage between:

Batch input

DDS reference

Transformation

Output product

Spreadsheets cannot manage this reliably at scale.

4. The Simplified Regime for Micro or Small Primary Operators

Another significant addition is Article 4a .

Micro or small primary operators:

Do not submit full DDS

Submit a one-time simplified declaration

Receive a declaration identifier

May replace geolocation with postal address (under specific conditions)

This is a thoughtful simplification, especially for low-risk countries.

But from a systems perspective, it creates a new data flow:

Instead of referencing a DDS, downstream actors may now reference a declaration identifier.

That distinction must be structurally embedded in traceability systems.

From my experience, once companies understand that audits are percentage-driven and risk-based, compliance becomes an operational necessity, not a reputational one.

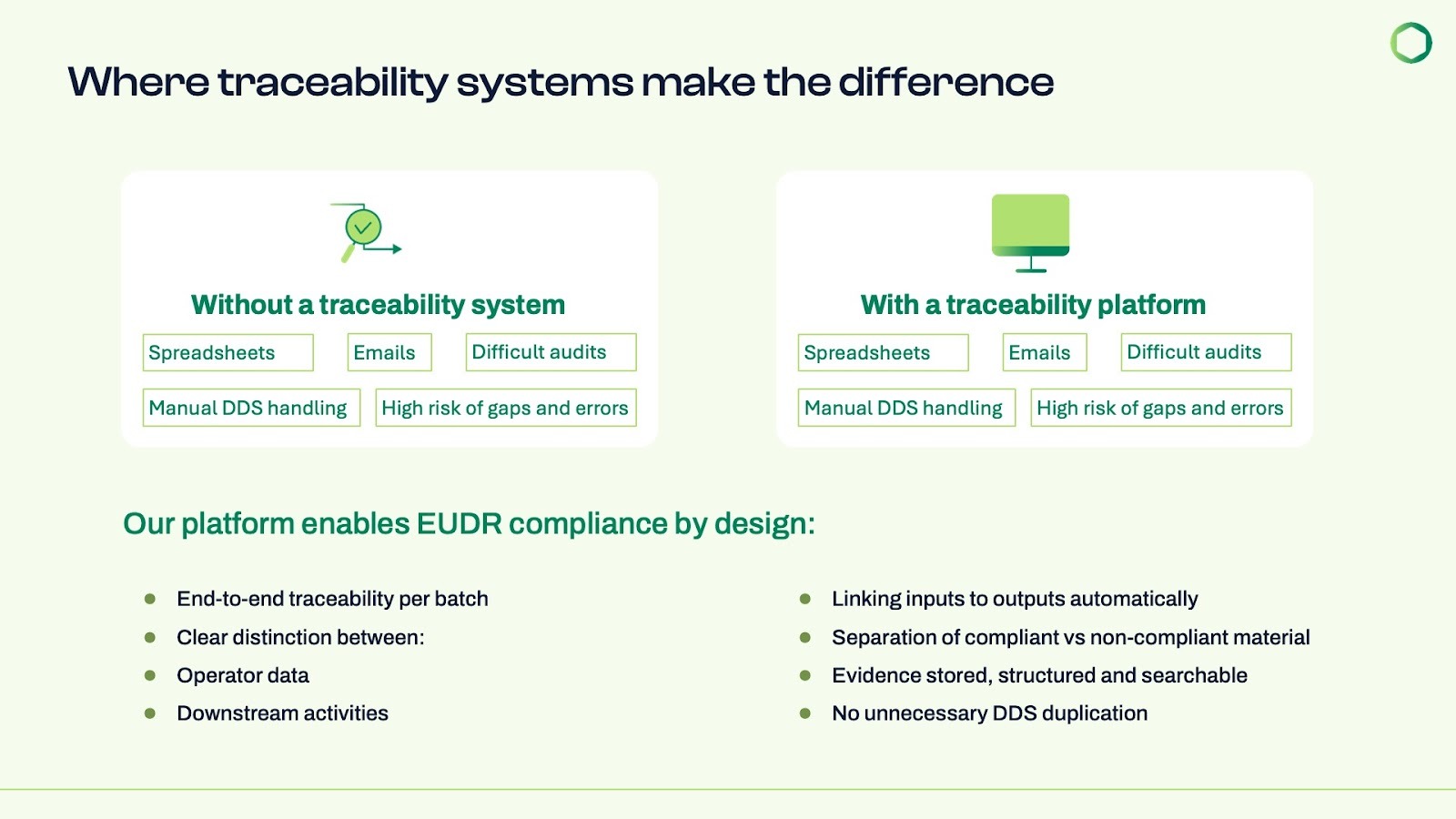

6. What This Means Operationally

After leading EUDR assessments, I consistently see five structural gaps:

No clear role mapping across entities in the group

No segregation logic preventing mixing of compliant and non-compliant material

No automated linkage between DDS references and batch outputs

No integration with TRACES / Information System

No structured five-year record retention

The amended Regulation does not change these needs.

It only clarifies who must perform which step.

7. Why Integrated Traceability Is Not Optional

At Finboot, MARCO Track & Trace was built for regulated industrial supply chains where:

Mass balance must be controlled

Inputs and outputs must be linked

Compliance must be automated

Evidence must be structured

Our EUDR module also provides:

API-based integration with the Information System

Secure storage of DDS reference numbers and declaration identifiers

Batch-level linkage

Automated alerts when new information indicates non-compliance (as required under Article 4(5) and Article 5(5))

In our Evonik project, the challenge was not only sustainability reporting. It was data integrity across transformation steps.

Compliance becomes scalable only when it is embedded in process, not managed as documentation.

MARCO Track & Trace automates EUDR compliance, Manage the full cycle —from supplier data collection, to deforestation risk assessment and monitoring to automated reporting of DDS to TRACES— all in one platform. No need for multiple tools.

Download our EUDR One-Pager:

8. A Final Reflection

Amended EUDR was framed as a simplification.

It is, legally.

But operationally, it is a refinement.

It clarifies:

Who does what

When

Through which system

Under which audit thresholds

Companies now have clarity.

The question is whether they use this clarity to build systems, or to delay action.

Reach out if you want to learn more about Evonik use case and explore how can we help you to comply with the EUDR in time:

Frequently Asked Questions (EUDR 2026 Update)

1. When does EUDR apply after Regulation (EU) 2025/2650?

From 30 December 2026 for most operators and traders, and from 30 June 2027 for natural persons and micro/small undertakings established by 31 December 2024 .

2. What is a downstream operator under the amended EUDR?

A natural or legal person placing on the market or exporting products made using relevant products already covered by a DDS or simplified declaration .

3. Do downstream operators submit DDS?

No. The amended Regulation removes that obligation .

4. Who must collect DDS reference numbers?

Only the first downstream operator or trader .

5. What is a micro or small primary operator?

An operator producing its own relevant commodities in a low-risk country, eligible for a simplified one-time declaration .

6. Can geolocation be replaced by postal address?

Yes, for micro or small primary operators under Article 4a(5) .

7. Are audits risk-based?

Yes. Minimum annual check percentages are defined by risk category .

8. Do penalties apply to downstream operators?

Yes. Penalties apply to operators, downstream operators and traders .

9. Is TRACES integration mandatory?

Reference numbers must be made available before customs release .

10. Does EUDR still require full traceability?

Yes. Simplification does not remove traceability requirements.

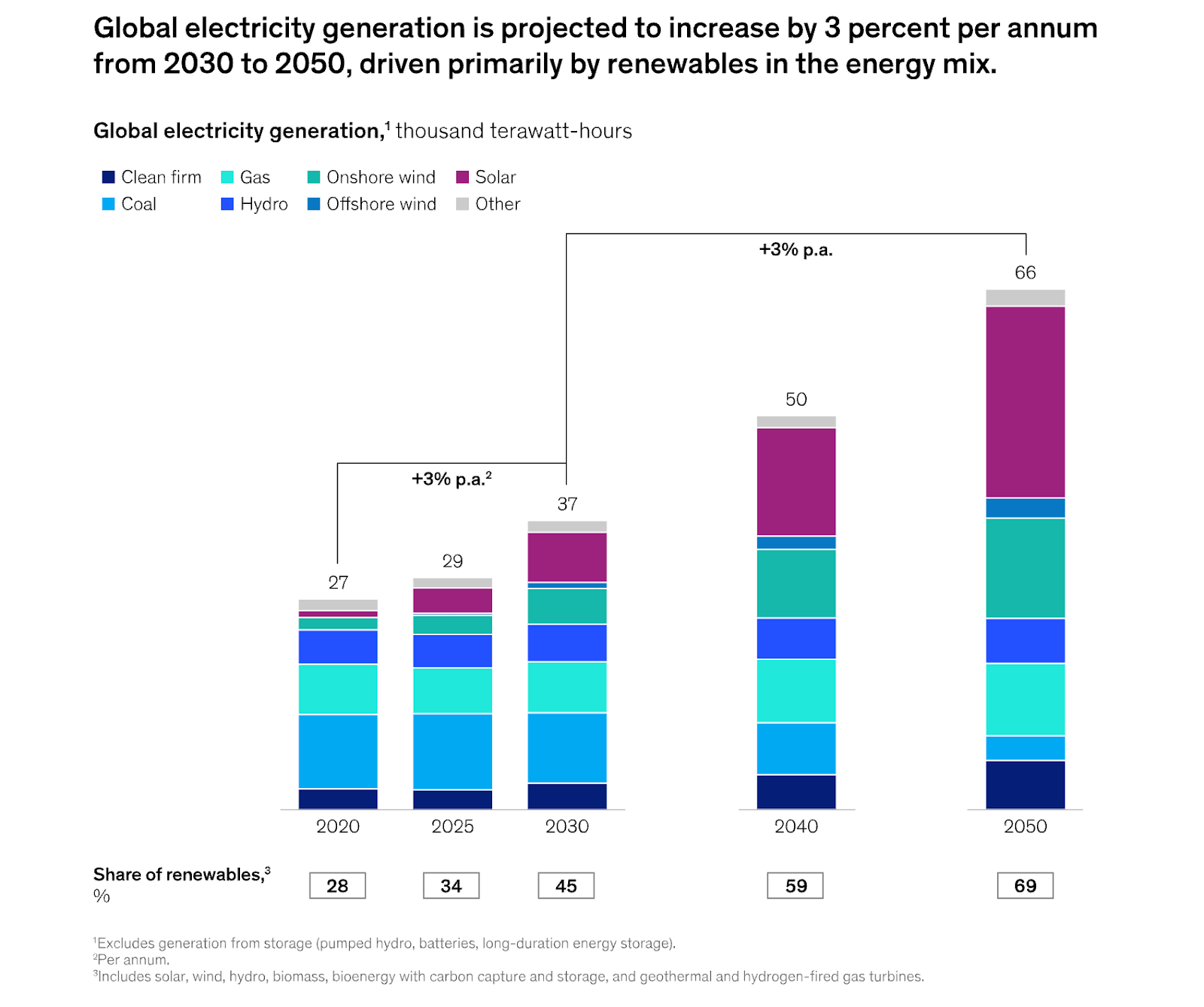

For years, decarbonization had been framed as an energy problem. With the solution driven by more renewables and more electrification. But this mindset was only focused on transforming the source of the resource and not the optimization of its consumption; a recent analysis from McKinsey makes a compelling point for the latter.

Software, particularly energy management systems, is emerging as the hidden catalyst of the global shift toward cleaner energy. As renewable energy scales and electricity becomes a larger share of global energy demand, managing volatility, flexibility, and optimization is no longer optional. It is foundational.

By 2040, renewable sources are expected to account for around 60% of global electricity generation, driven primarily by wind and solar. Electrification alone could reduce emissions by nearly 20% between 2024 and 2030. This is a much needed structural shift in how energy is produced; but energy is only one part of the decarbonization story.

Decarbonization is not just about replacing fossil fuels with electrons. It is about redesigning how economies source, transform, move, and verify value in a world where resources are constrained, geopolitics is volatile, and trust is fragile.

If we can learn anything from recent, and not so recent, history, it is that geopolitical events around energy (oil, gas, and other critical natural resources) shape power, trade, and stability. This will likely continue to be the case for our electrified future. The difference is that renewable energy systems — with their distributed generation, complex supply chains for critical minerals, and multi-jurisdictional sourcing — require a new kind of infrastructure to manage this complexity: digital infrastructure.

Software is what enables us to trace where materials come from, verify sustainability claims across borders, and maintain trust when physical supply chains span dozens of partners and jurisdictions. Just as energy management systems have become essential to optimize electricity consumption in real-time, digital traceability tools are becoming essential to manage the complexity of decarbonized supply chains — particularly for tracking renewable feedstocks, critical minerals, and the carbon footprint embedded in every transformation step.

From Climate Ambition to Business Risk

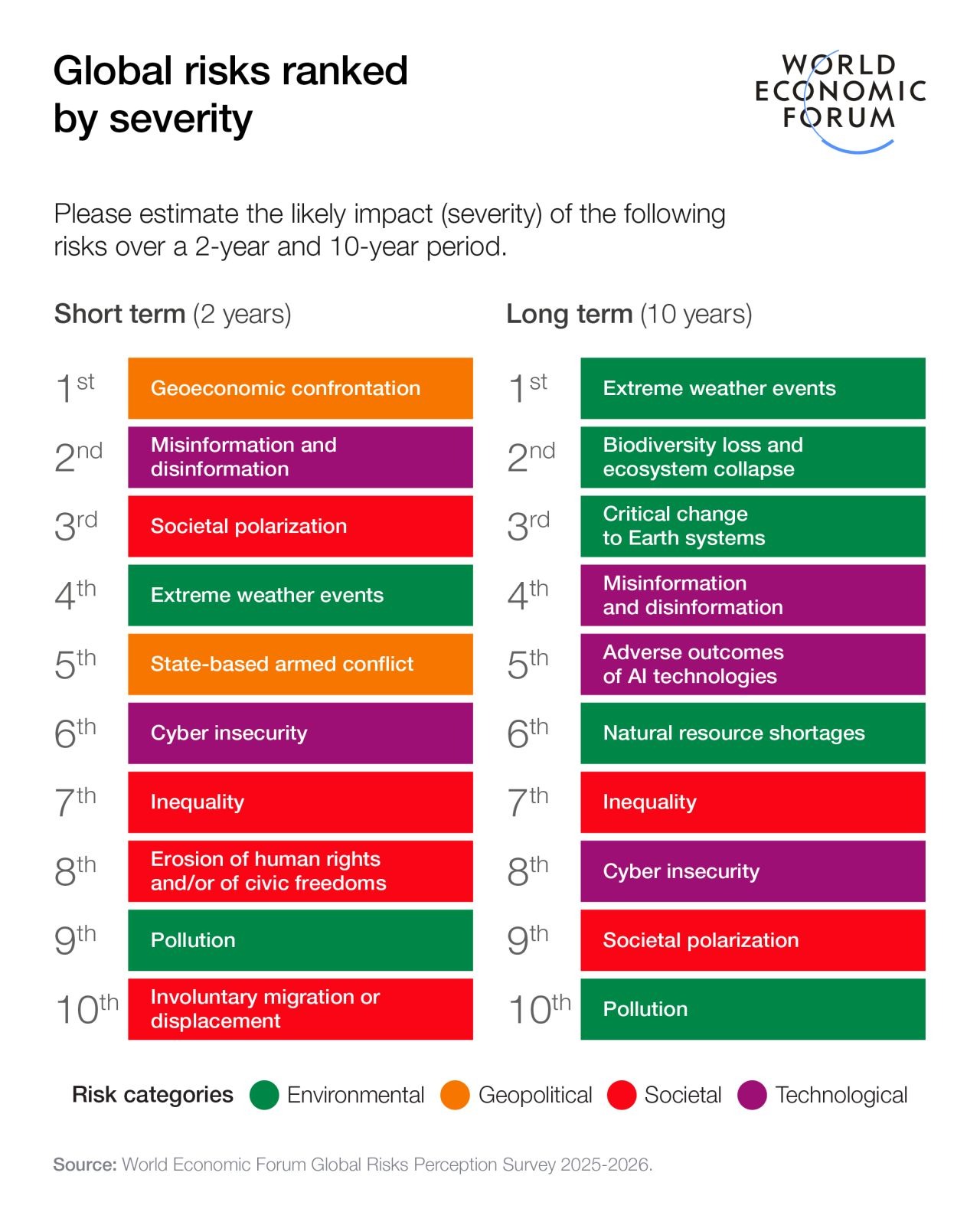

The World Economic Forum's Global Risks Report 2026 signals a critical shift in how business leaders view sustainability. Business leaders are worried about geoeconomic confrontation and misinformation in the short term, and extreme weather events and biodiversity loss in the long term.

They're business risks that directly impact supply chains, market access, capital costs, and regulatory compliance.

When weather events disrupt suppliers, when regulations demand verified sustainability claims, when investors require carbon data across your entire value chain, you need systems that provide real-time visibility and trusted data.

This is why digital traceability tools are becoming strategic infrastructure for risk management and mitigation. Just as energy management systems optimize electricity use, traceability systems help companies manage Scope 1, 2, and 3 emissions across complex global value chains — tracking renewable feedstocks, verifying mass balance, and substantiating claims.

Because sustainability is no longer a "moral" conversation. It is a conversation about business continuity, capital allocation, and long-term resilience — and it requires the right digital tools to execute.

Why Software Matters: Industrial Sectors as Part of the Solution

McKinsey makes a great point on the importance of energy management systems and their role in decarbonization. But what I explore in this article is why this matters beyond power grids.

Electrification is key, but electrons alone are not enough to meet our decarbonization goals, especially in hard-to-abate industrial sectors. Meaningful progress requires a broader energy mix (hydrogen, bioenergy, or recycled materials) and circular supply-chain strategies that address both emissions and resource efficiency.

Considering its significant need for energy, the industrial sector is often seen as the core responsible of the climate crisis, rather than as a crucial actor as part of the solution.

This matters because capital intensive sectors (like oil & gas, chemicals, steel, cement, manufacturing) are where the decarbonization challenge is most acute. And these sectors share something critical with the broader supply chain challenge: they require verified data, transparency across complex processes, and trust in the attributes being tracked.

The lesson from energy management systems extends far beyond the factory gate or the building meter.

If software is essential to manage the complexity of distributed energy systems, the same logic applies, and perhaps even more urgently, to the broader challenge of industrial decarbonization and supply chain transparency.

The real complexity sits across global supply chains, multi-tier sourcing networks, mass balance models, regulatory regimes, and sustainability claims that must be verified, not asserted. When we move beyond the boundaries of a single site or grid connection, many decarbonization strategies begin to lose coherence.

Supply chains remain fragmented. Sustainability data is scattered across organizations and systems that were never designed to work together. Claims are made upstream that cannot be verified downstream. Decisions are delayed because confidence in the data is missing.

This is where many decarbonization strategies begin to break down.

Companies invest heavily in measuring emissions, only to discover that data is fragmented across systems and partners, assumptions cannot be verified, claims cannot be defended, and decisions are made too late.

You cannot decarbonize what you cannot trace, contextualize, and trust.

Beyond Carbon Accounting: From Reporting to Operating

Carbon accounting has become a central focus, and rightly so. Regulation demands it. Investors expect it.

But on its own, it is insufficient.

Carbon data is often backward-looking, aggregated, and disconnected from operational decisions. It tells us what has already happened, often too late to influence outcomes.

Decarbonization, in practice, happens through thousands of daily choices: which supplier to source from, which feedstock to prioritize, which process to adjust, which claim can be made (and which cannot).

This is where software becomes transformative: not as a reporting layer, but as operational infrastructure.

Transparency enables optimization. Trusted data enables action. Systems enable scale.

Decarbonization accelerates when sustainability data is embedded directly into how supply chains operate, not added at the end.

Traceability as Strategic Infrastructure

At Finboot, we see this shift clearly, particularly in the hard-to-abate industrial sectors where the challenge is most acute.

Digital traceability is no longer a niche requirement driven by regulation alone. It is becoming core infrastructure for managing risk, trust, and resilience in complex industrial ecosystems.

Just as McKinsey highlights the importance of digital twins for optimizing energy use in production processes, we use digital twins in our blockchain-based traceability solutions to enhance supply chain transparency. These digital twins enable companies to back up sustainability claims — including carbon footprint, mass balance integrity, and digital product passports — with verifiable data at every transformation step.

When traceability is treated as infrastructure rather than as a compliance layer, its impact changes fundamentally. Transparency stops being a communications exercise and becomes a management capability. Sustainability data stops being cosmetic and becomes strategic.

Traceability enables companies to verify sustainability claims with confidence, maintain data integrity across transformations, respond faster to regulatory and market demands, and reduce exposure to sourcing, compliance, and reputational risk.

Most importantly, it creates a single source of truth across organizations that do not fully control their value chains.

This is not about technology for its own sake. It is about governance.

In an environment where resources are contested, regulation is accelerating, and markets reward credibility over promises, trust and transparency become strategic assets.

Energy, Supply Chains, and the Next Phase of Decarbonization

McKinsey is right: software is the hidden catalyst for decarbonization.

At Finboot, we see this reality daily in our work with companies operating in complex value chains involving renewable feedstocks, bio-based products, and regulated materials. In these sectors, the challenge is rarely a lack of data. The challenge is fragmentation, inconsistency, and trust.

When we implement a digital traceability backbone, the transformation goes beyond better reporting:

Data can be shared securely across partners.

Sustainability attributes can be verified at each step.

Claims can be substantiated, not assumed.

Decision-makers gain real-time visibility into risk and performance.

The result is better control, better decisions, and greater trust across the ecosystem. This is what software enables when it is designed as infrastructure, not as a dashboard — when it serves as the connective tissue between operational reality and strategic intent.

Decarbonization will not be delivered by isolated tools or standalone metrics. It will be delivered by integrated digital infrastructures that connect energy, materials, data, and trust across organizational boundaries.

Electrification without traceability creates blind spots. Renewables without governance create volatility. Ambition without systems creates risk.

The organizations that succeed will be those that treat decarbonization as a systems redesign challenge, not a compliance exercise.

And just to wrap this up…From where I sit, three principles are becoming clear:

Decarbonization is a data strategy. Not because data is fashionable, but because decisions without trusted data are liabilities. In hard-to-abate sectors — chemicals, steel, cement, biofuels — the ability to trace feedstock origins, verify transformation processes, and substantiate sustainability claims determines which companies can compete in increasingly regulated markets. Companies that recognize this are already moving beyond compliance toward strategic resilience.

Transparency is infrastructure. Not a communication tactic. Not a report. Infrastructure. When sustainability data is treated as a management capability rather than a reporting obligation, its strategic value becomes unmistakable. It enables faster response to regulatory requirements, reduces exposure to greenwashing risk, and creates the foundation for credible market differentiation.

Resilience beats efficiency. The most optimized supply chain is not the most resilient one. Highly optimized supply chains may perform well under stable conditions, but they fracture under volatility. Software-enabled transparency allows organizations to balance both: 1) to adapt faster, manage risk earlier, and 2) make decisions with greater confidence when conditions change.

Geopolitics is reminding us (once again) that resources matter. Climate risk is reminding us that stability cannot be assumed. Markets are reminding us that trust has tangible value.

The companies that internalize this will not only comply faster but also they will compete better.

And in the decade ahead, that distinction will matter more than ever.

Software is not the story. But without it, none of the rest holds together. And that may be the most underappreciated reality of the decarbonization transition ahead.

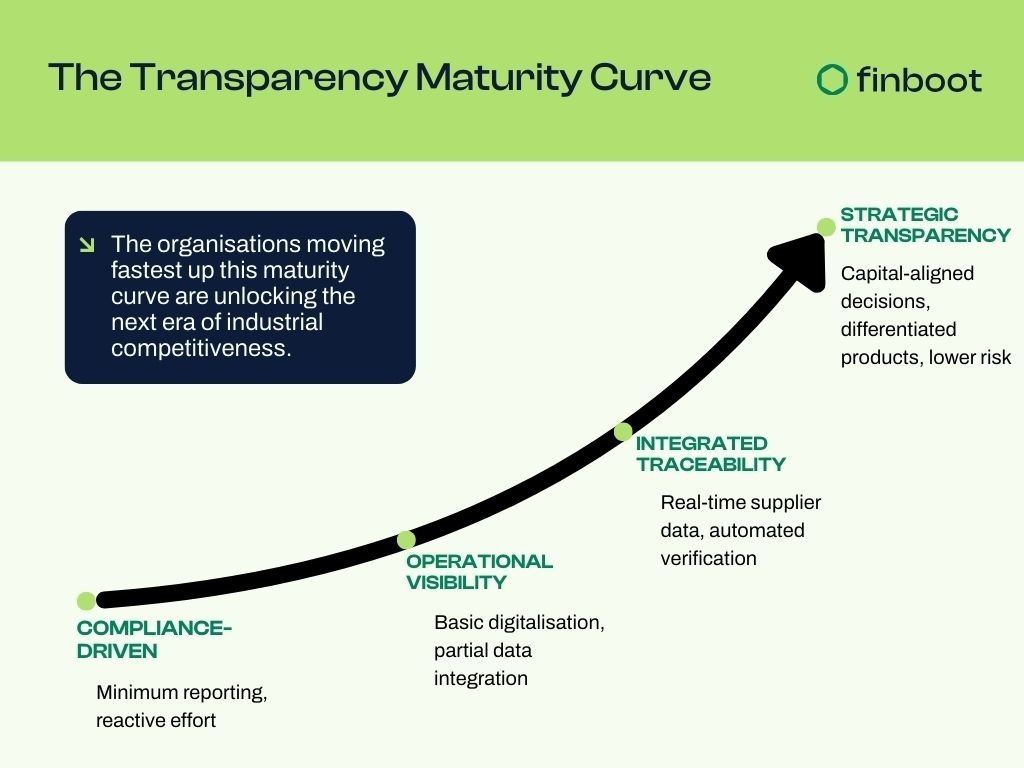

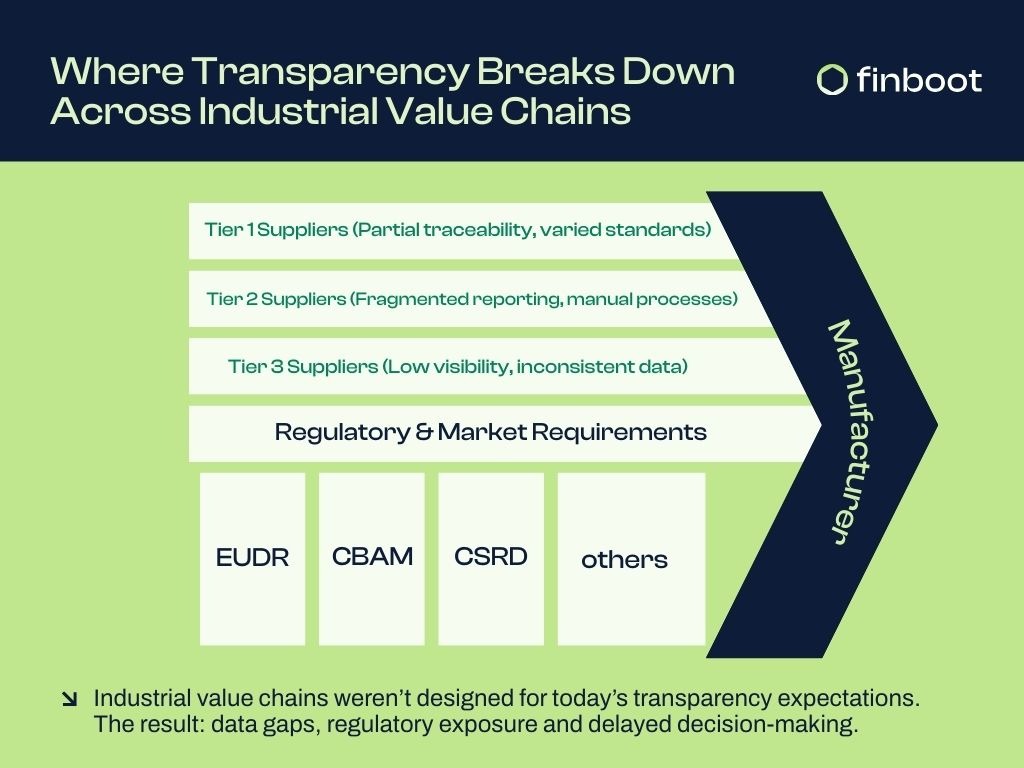

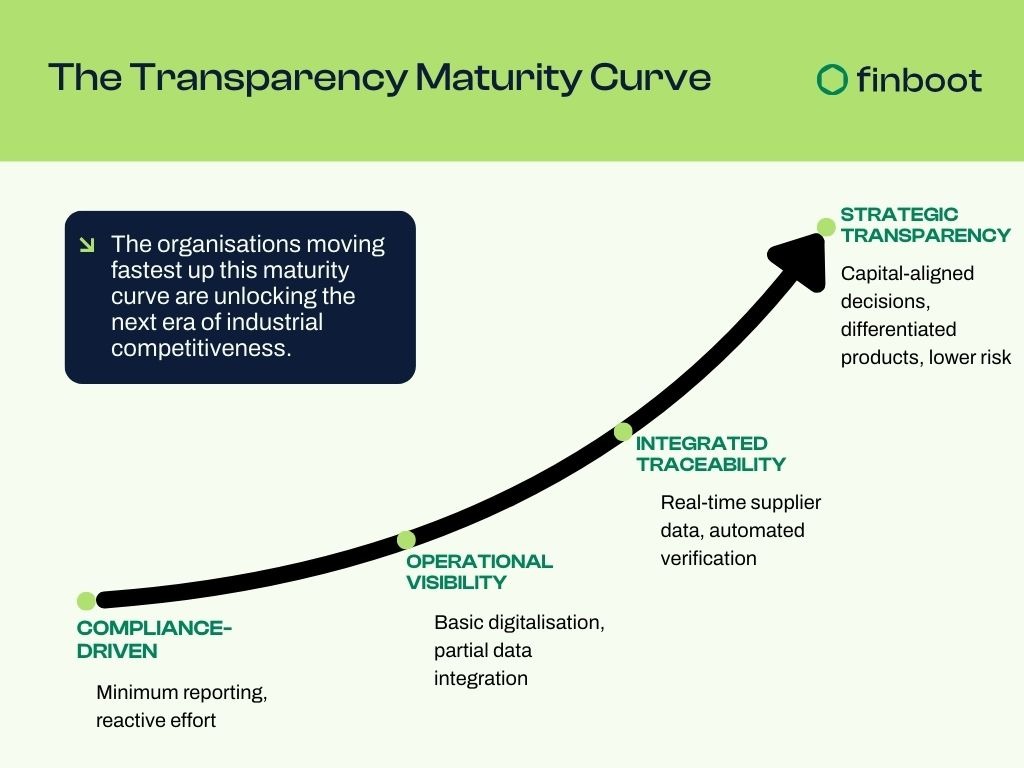

For more than a decade, transparency in heavy industries has been treated as an operational concern: a data challenge for sustainability teams or a compliance workflow to satisfy evolving reporting regimes. But that framing no longer matches the realities facing industrial leaders. As regulatory timelines accelerate and value chains become more exposed to disruption, transparency has quietly moved from the periphery of corporate agendas to the centre of boardroom strategy. In today’s environment, transparency is directly shaping how companies deploy capital, manage structural risk and evaluate pathways for growth.

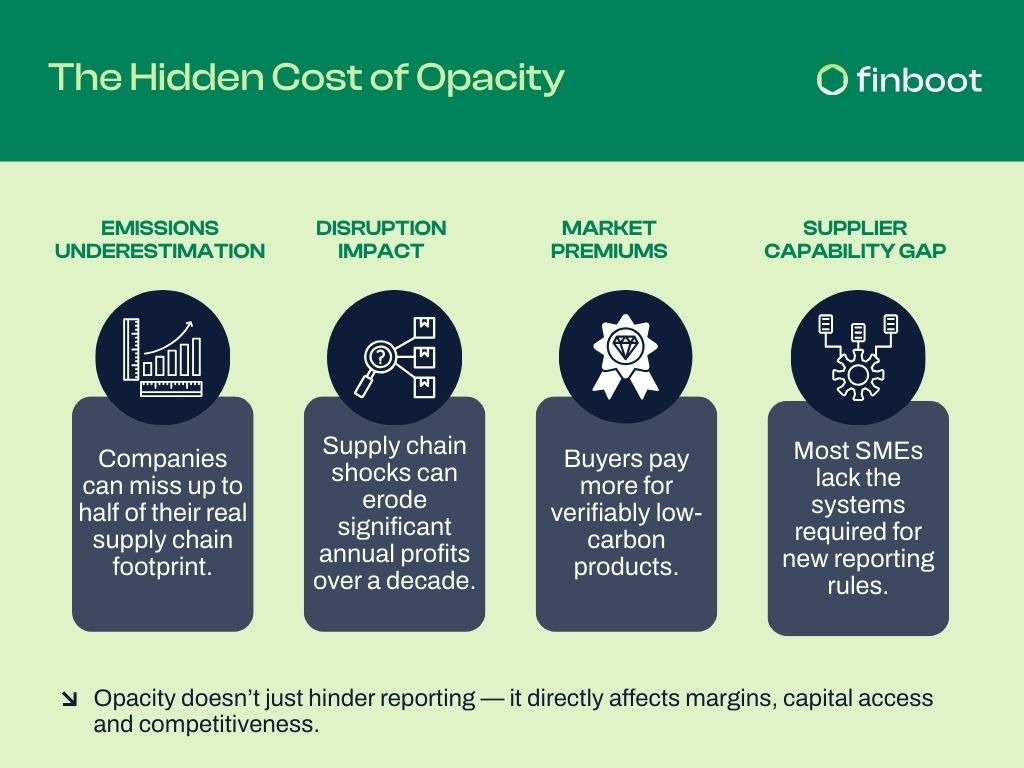

One reason for this shift is the increasing financial cost of opacity. According to CDP, companies with incomplete supply chain data underestimate their emissions by around 50% (CDP Supply Chain Report). This blind spot has material consequences. The European Union’s emerging regulatory frameworks—from the Corporate Sustainability Reporting Directive (CSRD) to the EU Deforestation Regulation (EUDR) and the Forced Labour Regulation (EU Forced Labour Regulation)—now link supply chain transparency directly to market access, financial exposure and credibility. Missing or unverifiable supplier information is already slowing investment decisions and undermining capex planning, particularly in sectors such as steel, chemicals and mining where margins are thin and asset replacement cycles are long.

The World Economic Forum estimates that supply chain disruption costs companies an average of 45% of one year’s EBITDA over a decade (WEF Global Risks Report). When opacity amplifies this volatility, the cost is strategic, not administrative.

Opacity also narrows a company’s ability to differentiate at a moment when markets increasingly reward verifiable sustainability performance. Research from McKinsey shows that B2B buyers are now willing to pay 5–20% premiums for products with demonstrably lower carbon intensity or traceable origins (McKinsey: The case for green products). Without credible transparency, companies are pushed into competing solely on price in sectors where price competition is already severe.

Yet the greatest structural bottleneck remains supplier engagement. Heavy-industry value chains depend on SME suppliers that often lack digital tools, standardised reporting frameworks and internal expertise. The OECD notes that more than 70% of SMEs feel unprepared to meet new sustainability reporting requirements—not due to unwillingliness but due to capability gaps (OECD Green & Digital Transformation of SMEs). This misalignment creates friction precisely where resilience is most needed. When transparency is positioned as a compliance burden, resistance is natural. But when it is positioned as a mechanism for suppliers to access new markets, secure longer-term contracts or qualify for sustainability-linked finance—an IFC priority area forecasted to exceed $1 trillion annually by 2030 (IFC Sustainability-Linked Finance Market)—the dynamic fundamentally shifts.

For executive teams, the return on transparency is therefore multidimensional. It reduces exposure by making regulatory and operational risks visible earlier, allowing leadership to avoid costly surprises. It improves capital efficiency by strengthening eligibility for sustainability-linked loans and reducing risk premiums associated with opaque value chains. It enhances competitiveness by enabling credible differentiation in markets that increasingly reward verifiable performance. And perhaps most importantly, it restores strategic optionality—the ability to pivot sourcing models, enter new markets, redesign product portfolios or allocate capital with confidence because the underlying data is trustworthy.

This is also why digital traceability is emerging not as another tool but as infrastructure. Just as ERPs became foundational to finance and logistics platforms became essential to global operations, traceability systems are becoming the backbone of sustainability, compliance and supply chain orchestration. They connect fragmented data flows across suppliers, transform manual reporting into real-time verification and enable organisations to turn regulatory pressure into strategic clarity.

Across industries, we are already seeing how organisations that treat digital transparency as infrastructure unlock resilience and measurable value. In sustainable chemicals, for example, Moeve has implemented end-to-end traceability across its palm-oil supply chain to support the launch of its first sustainable LAB, automating mass balance processes, improving data accuracy and strengthening customer trust through transparent product passports. In the circular materials sector, SABIC has achieved batch-level traceability from waste feedstock to packaging, enhancing the credibility of chemical recycling, reducing audit burdens and reinforcing accountability with partners as recycled content scales. In specialty chemicals, Evonik has adopted a fully digital, auditable approach to compliance with deforestation-free sourcing requirements, automating supplier documentation and geolocation risk checks to ensure that palm-oil-based ingredients meet strict regulatory thresholds. And in the energy industry, the partnership between Finboot and Sendero demonstrates how synchronising field-verified methane measurements with blockchain-enabled traceability creates an end-to-end auditable workflow that not only meets methane reporting standards but also unlocks premium market opportunities and carbon-credit revenues.

Together, these examples reveal a structural pattern: when transparency becomes embedded as core infrastructure, organisations move beyond compliance to shape competitive advantage. They gain the ability to operate with speed, certainty and credibility in markets defined by constraint. Ultimately, transparency is no longer a technical exercise — it is a leadership decision. And the companies willing to act on that decision today will be the ones defining industrial competitiveness tomorrow.

Ultimately, transparency is no longer a technical exercise—it is a leadership choice. And the companies willing to act on that choice today will be the ones defining what competitiveness looks like tomorrow.

Empowering professionals to turn ESG knowledge into strategic value through practical, technology-driven learning.

Barcelona, Spain & London, United Kingdom — October 17, 2025. Finboot, a leader in green supply chain management solutions, today announces it will be part of a new educational program, “Data & AI for Sustainability Reporting” in partnership with Skills4Impact. The five-week course, starting 12 November, equips professionals with the skills to collect, analyze, and report ESG (environmental, social, and governance) data efficiently and strategically, combining global standards with the potential of AI and digital tools.

Bridging the Attitude-Behavior Gap in Sustainability

Although 90% of executives recognize the importance of sustainability, a BCG/MIT study reveals that only 60% of companies incorporate sustainability into their business strategy, and a mere 25% have embedded it into their business model. Additionally, 75% of corporate sustainability professionals believe businesses need to improve their strategic approach to meet pressing global mega-trends, according to Silicon Luxembourg. This gap between awareness and action underscores the urgent need for rigorous sustainability education programs that empower professionals to drive measurable impact across organizations.

The role of the Chief Sustainability Officer (CSO) is a clear reflection of this shift. According to the Harvard Business Review, CSOs are moving from roles focused on communication and reputational risk to strategically integrating ESG into corporate decision-making. Today’s CSOs collaborate closely with senior leadership and investors, helping companies prioritize ESG issues with the greatest financial and operational impact. This transformation demands skilled professionals who understand both sustainability frameworks and the technological tools needed to implement them effectively.

Building a Comprehensive Sustainability Learning Ecosystem

This program is part of Finboot’s broader commitment to sustainability education, designed to bridge the gap between awareness and actionable business strategy. Recognizing that companies often struggle to translate sustainability ambitions into measurable outcomes, Finboot has built a comprehensive ecosystem of learning resources for professionals seeking to drive change across their organizations. These initiatives include the Finboot Dictionary, a series of short videos explaining key concepts in sustainability, digital traceability, and technology; the Green Supply Chain Insights web series, hosted by Finboot’s CEO and co-founder, offering practical perspectives on sustainable supply chains; and Green Supply Chain Talks, expert interviews that explore sustainability, technology, and supply chain strategy in depth.

Finboot also hosts the Green Supply Chain Loop podcast on Spotify, consolidating insights from videos, talks, and webinars into a weekly conversation with leaders driving transparency and responsible business practices. In addition, Finboot produces blogs, eBooks, and masterclasses on topics such as navigating European sustainability regulations. Most recently, the company delivered a masterclass at Climate Week NYC and will continue with sessions during Circular Economy Weeks in ReLondon and Mazovia.

Why the New Course Matters

Sustainability reporting requires rigor, accuracy, and strategic insight—areas where many organizations struggle. According to KPMG (2024), 47% of companies still use spreadsheets for ESG data management, which prevents the delivery of reliable and verifiable metrics. Furthermore, an IBM report (2024) found that 56% of companies have not yet applied artificial intelligence to improve their sustainability performance, and only 30% recognize an improvement in the accuracy of sustainability reports due to the implementation of new technologies. “Data & AI for Sustainability Reporting” equips participants with the frameworks, methodologies, and tools to generate reliable, traceable, and actionable sustainability reports, aligning ESG performance with business strategy.

“Sustainability is no longer a peripheral responsibility—it is central to corporate growth, resilience, and value creation,” said Juan Miguel Pérez, CEO of Finboot. “Through our comprehensive education ecosystem, we aim to give professionals the knowledge and tools to make informed, strategic decisions. From micro-learning videos to in-depth courses and masterclasses, our goal is to transform awareness into measurable business impact.”

“Professionals are eager for practical, technology-driven ESG training,” added Flávia Sales, Marketing Manager of Finboot. “Our role in this program is to make complex sustainability concepts such as Digital Product Passport, GHG Tracking and Mass Balance, accessible and actionable, turning ambition into measurable impact.”

About Finboot

Finboot is a Green Supply Chain Management company helping energy, chemical, and manufacturing leaders automate and scale traceability across complex supply chains. Our flagship solution, MARCO Track & Trace, enables companies to gather, verify, and share supply chain data to back up ESG claims, reduce emissions, and meet regulatory requirements including EUDR, ESPR, and CBAM. With unmatched configurability, Finboot fits around your existing processes—empowering operational efficiency, unlocking value from sustainable products, and adapting to evolving business needs. Our customers include SABIC, Evonik, Repsol, and Moeve.

The European Parliament and the Council have reached a provisional agreement to update the EU Waste Framework Directive (WFD). While the WFD has long been a cornerstone of European waste policy, this targeted amendment represents a major turning point—especially for the textile sector.

From 1 January 2025, Member States must have ensured separate collection of textile waste, backed by new obligations for producers under mandatory and harmonised Extended Producer Responsibility (EPR) schemes. This is not just an incremental policy shift; it represents a fundamental change in how products are designed, consumed, and managed throughout their lifecycle.

What Is Extended Producer Responsibility (EPR)?

At its core, Extended Producer Responsibility (EPR) is about accountability. It shifts the burden of end-of-life product management away from governments and taxpayers, and onto the companies that place products on the market.

Rooted in the internationally recognised “polluter pays” principle, EPR ensures that the true cost of waste—collection, sorting, recycling, disposal—is borne by those who profit from the production and sale of goods.

While already established in areas such as electronics, batteries, and packaging, the EU’s new rules extend EPR to textiles, with several important implications:

Producers will finance collection, sorting, reuse, and recycling of textiles.

Eco-modulation of fees will reward companies that design products with higher circularity (e.g., use of recycled fibres, durability, or recyclability).

A wide range of textile products are covered, including clothing, footwear, hats, curtains, blankets, and household linens.

E-commerce platforms and non-EU producers selling into the EU will also be subject to EPR rules, closing loopholes that previously left overseas sellers unaccountable.

Stricter rules on waste shipments will reduce the risk of textile waste being exported under the false label of “reuse.”

This approach not only tackles Europe’s growing textile waste problem but also incentivises circular business models and product design innovation.

The Bigger Picture: Food Waste and Beyond

The amendment agreed on 18 February 2025 also touches on other waste streams. For instance, binding food waste reduction targets now require:

A 10% reduction in food waste from processing and manufacturing.

A 30% per capita reduction from retail, restaurants, food services, and households by 2030.

Although the EU is setting the pace, EPR is going global.

In theUnited States, for example, there are already 146 EPR laws across 35 states, covering 21 product categories—and that number is only expected to grow. Packaging laws are moving fastest, with states like California, Oregon, and Colorado taking the lead. California’s SB 54 requires manufacturers to register, report packaging data, and take steps to reduce plastic pollution, while Oregon’s SB 582 makes participation in Producer Responsibility Organisations (PROs) mandatory and requires regular disclosure of product impacts. For companies operating in multiple states, this creates a fragmented landscape that demands proactive planning and close collaboration with suppliers to track sustainability data across jurisdictions.

The United Kingdom has also been tightening its EPR rules for packaging. Businesses that supply or import packaging above certain thresholds now need to report their packaging data, pay recycling and waste management fees, and ensure they meet all compliance requirements. Large organisations must keep detailed records of the packaging they supply or import, pay relevant fees, and submit reports every six months. Smaller organisations also need to track and report their data, with the first submissions having been due on April 1, 2025. The rules cover a wide range of activities, including supplying packaged goods under your own brand, importing packaged products, running an online marketplace, providing reusable packaging, or supplying empty packaging.

For multinational companies, keeping up with these regulations can be challenging. The key is having reliable processes to collect and share data across the supply chain, staying closely connected with suppliers, and keeping track of obligations in every market. Companies that manage this well can not only stay compliant but also use it as an opportunity to strengthen their sustainability efforts and gain a competitive edge.

Why EPR Matters for Businesses

EPR regulations aren’t just about compliance—they reshape business strategy at every level:

Financial Impact: Producers will face new compliance fees, contributions to waste management programs, and administrative costs. Eco-modulation also means that poor design choices can become more expensive over time.

Operational Complexity: Managing EPR across multiple jurisdictions will demand robust data systems and collaboration across suppliers. Companies will need to integrate compliance reporting into procurement, product design, and logistics.

Product Design and Innovation: EPR pushes manufacturers to design for circularity—from material selection to recyclability. This could drive a new wave of product innovation, especially when combined with the Ecodesign for Sustainable Products Regulation (ESPR). ESPR complements EPR by setting clear sustainability requirements—particularly for textiles (especially apparel), steel, and aluminium—including durability, repairability, reusability, energy and resource efficiency, recycled content, and transparency on carbon footprints.

How Digital Traceability Turns EPR Compliance into Opportunity

Extended Producer Responsibility (EPR) brings new obligations for companies: tracking products, financing collection and recycling, and ensuring compliance across multiple jurisdictions. For organizations with complex supply chains, meeting these requirements can be overwhelming—different rules, extensive reporting, and rising administrative costs.

Finboot’sMARCO Track & Tracesimplifies this challenge. Its Digital Product Passport (DPP)—a blockchain-verified digital twin for every product—carries all essential information about sustainability, compliance, and performance throughout the product lifecycle.

Compliance records: EPR obligations, along with regulatory frameworks like RED III, CSRD, and others.

Immutable, auditable proof of every step in the supply chain.

While the DPP is mandatory under ESPR, it also becomes a powerful tool to meet EPR requirements. Companies can generate and manage DPPs across batches, share them automatically with stakeholders, and customize the data depending on the audience. This ensures that internal teams, suppliers, and customers all have the information they need—while staying fully compliant.

With MARCO Track & Trace, compliance transforms from a burden into a streamlined, automated process:

Sustainability reports generated automatically, saving time and resources.

Compliance documents linked directly to product data.

Audits reduced from weeks of preparation to a few clicks.

Full transparency across supply chains, enhancing trust with regulators, partners, and consumers.

By embedding compliance into the Digital Product Passport, MARCO T&T turns EPR from a regulatory headache into an opportunity for efficiency, transparency, and innovation. Companies that embrace this approach can not only comply but differentiate themselves in a market increasingly driven by sustainability and circularity.

With MARCO Track & Trace, EPR compliance is not just achievable—it’s a competitive advantage. Contact us here.

___________________________

FAQs

What products are covered under the new EU EPR rules for textiles?

The rules apply to a wide range of textile products, including clothing, footwear, hats, curtains, blankets, and household linens. Both EU-based and non-EU producers selling into the EU are subject to these obligations.

How does EPR affect product design and sustainability strategies?

EPR encourages companies to design products for circularity. This means prioritizing recycled materials, durability, repairability, and recyclability. Eco-modulated fees reward manufacturers who make more sustainable choices, aligning financial incentives with environmental impact.

Can digital traceability help with EPR compliance?

Yes. Digital Product Passports (DPPs) like those provided by Finboot’s MARCO Track & Trace platform provide a blockchain-verified record of every product’s lifecycle. This enables companies to track sustainability data, manage regulatory obligations, generate automated reports, and simplify audits, turning EPR compliance into a strategic advantage.

Are EPR regulations only relevant in the EU?

No. While the EU is leading the way, EPR is becoming a global trend. The U.S., U.K., and other countries are implementing similar regulations, particularly for packaging and electronics. Companies operating internationally must stay updated on each jurisdiction’s requirements and maintain robust supply chain data.

London, UK – Minneapolis, US, MONDAY 7th OCTOBER 2025 – BanQu, the award-winning supply chain traceability platform, and Finboot, a pioneer in green supply chain management technology, today announced a strategic partnership to accelerate “at origin” tracking, reporting, and verification using AI, blockchain, and advanced analytics.

As economic uncertainty continues globally, companies are trying to secure their supply chains and build “just-in-case” safeguards. While most companies know their tier 1 and tier 2 suppliers, they have little to no information or insight into the next set of tiers where rubber hits the road. This leads to higher sourcing costs, regulatory fines and disruptions.

The collaboration combines BanQu’s proven expertise in first-mile traceability and inclusion with Finboot’s industry-leading Green Supply Chain Management suite. Together, the companies will deliver an end-to-end solution that empowers enterprises to capture and verify data across their value chains—from raw material sourcing to the final consumer—while meeting the growing demands of regulators, investors, and conscious consumers.

BanQu has pioneered “origin track and trace” for millions of suppliers and processed over 9 billion kilos of commodities such as rice, barley, coffee, cocoa, oil palm, PET, glass, cassava, etc. since 2016.

Global consumer brands, international development banks, and trading companies use its patented blockchain & AI SaaS platform in their everyday sustainability and procurement operations to reduce costs and increase supply chain efficiencies.

Finboot’s technology provides supply chain management for the world’s leading companies. Its platform traces carbon emissions and minimizes risk through immutable data. Finboot has created the first green supply chain management suite with integrated traceability, enabling companies to track emissions, automate digital product passports, create sustainability credits, and facilitate compliance. Finboot operates across the UK, Europe, and the US with flagship customers such as Evonik, Repsol, Sabic, Moeve, Gestamp, and Big River Steel (a US Steel company), amongst others, and is backed by Sabic and Repsol.

By integrating BanQu’s mobile-first traceability tools with Finboot’s green supply chain suite, the partnership will:

· Enable companies to meet evolving regulatory reporting standards with confidence.

· Strengthen auditability and compliance across global supply chains.

· Empower producers, workers, and SMEs at the grassroots with digital inclusion.

· Provide investors and consumers with verifiable sustainability data.

Ashish Gadnis, CEO of BanQu, said, “This partnership with Finboot is a major step forward in our mission to democratize supply chains. By fusing accessibility with blockchain trust, we can drive measurable impact at both ends of the value chain.”

JuanMiguel Pérez, CEO of Finboot, added, “Together with BanQu, we are creating a powerful ecosystem where transparency, compliance, and sustainability go hand in hand, unlocking long-term value for businesses and society.”

Nish Kotecha, Chair of Finboot, added, “Our mission at Finboot is to harness technology for meaningful change. Partnering with BanQu extends that vision by combining trust, transparency, and inclusion. This collaboration creates a powerful opportunity for enterprises to meet ESG goals while driving real impact for people and the planet.”

–ENDS –

Notes to Editors

For more information, please contact nish@finboot.com or info@banqu.co

Tagline:“BanQu and Finboot—powering transparent, inclusive, and sustainable supply chains.”

About Finboot

Finboot’s technology supply chain management for the companies. Our technology traces carbon emissions and minimizes risk through immutable data. Finboot has created the first green supply chain management suite with features including integrated traceability, allowing you to track carbon emissions, automate digital product passports, create your sustainability credits, and facilitate compliance. Finboot is backed by SABIC and Repsol. Finboot is headquartered in London with a base in Barcelona.

BanQu is one of the first and largest end-to-end blockchain-based sustainability & procurement platforms that connects the first mile and last mile of complex supply chains seamlessly. Used in over 50 countries BanQu has connected over 6,000,000 beneficiaries, including SMEs, smallholder farmers, waste pickers, and artisanal miners, to global supply chains. Its platform is language, currency, and device agnostic. BanQu is headquartered in the USA with regional operations in Africa, Europe, and Asia.

Combining boots-on-the-ground measurement with blockchain-enabled traceability unlocks compliance, trust, and market advantage for oil & gas operators.

London, United Kingdom—September 9, 2025. Finboot, a leader in green supply chain management solutions, today announces a strategic partnership with Sendero Environmental & Well Services, an established environmental services provider with more than 30 years of oil & gas compliance expertise. Together, the companies will deliver an integrated, verifiable pathway from methane mitigation to high-integrity carbon accounting—enabling operators to transform emissions reductions into both regulatory assurance and financial value.

Closing the Measurement-to-Monetization Gap

For oil & gas operators, methane is not just a compliance challenge but also a financial lever. Accurate measurement and transparent reporting unlock access to carbon credits, satisfy domestic and international regulatory frameworks, and secure premiums in markets such as LNG exports to the EU, where buyers increasingly demand proof of lower-carbon supply.

Sendero brings decades of expertise in field-verified data collection, spanning valve and flange counts, high-flow sampling, optical gas imaging, GHG inventories, and CCUS MRV (Monitoring, Reporting, and Verification). This robust physical dataset is then secured through Finboot’s MARCO Track & Trace blockchain platform, ensuring data integrity, auditability, and compatibility with compliance and voluntary carbon markets for credit issuance, including frameworks like OGMP 2.0 and tariff mechanisms like CBAM.

From Compliance Burden to Market Advantage

The Sendero–Finboot partnership creates a reliable, auditable pathway from physical methane measurement to digital emissions traceability. By connecting field-level verification with blockchain-enabled transparency, operators can reduce compliance risk through verifiable, audit-ready data while unlocking new value. Emissions reductions can be monetized via carbon credits and sustainability-linked financing, and lower-carbon LNG can capture market premiums, strengthening customer loyalty and long-term export advantages. At the same time, operations are streamlined with integrated workflows that connect measurement, reporting, and verification into one trusted system.

This alignment of physical measurement and digital traceability transforms methane mitigation into a tangible business opportunity—turning what was once a cost center into a revenue stream and market differentiator.

"Methane mitigation is both a business necessity and a financial opportunity," said Juan Miguel Pérez, CEO of Finboot. “Companies need robust, field-verified tracking of their emissions, followed by the ability to trace, monitor, and report this data over time. Only then can they claim real reductions, demonstrate progress, and monetize saved emissions to generate a tangible return on sustainability investments. Partnering with Sendero allows us to connect these steps, transforming verified field data into a trusted pathway from methane mitigation to emissions monetization, strengthening compliance while unlocking new market opportunities.”

"When methane data is measured, verified, and traceable end to end, it becomes bankable. Together we turn field proof into audit-ready carbon accounting that enables credible credit issuance, premium offtake, and durable customer trust,” said David Stewart, President andCo-Founder of Sendero ESG.

About Sendero

Sendero partners with operators to solve their most pressing environmental and operational challenges. From emissions monitoring and compliance management to well plugging and site reclamation, Sendero delivers integrated solutions that reduce risk, ensure regulatory confidence, and unlock new opportunities such as carbon credit generation. With expertise across the full lifecycle—from pre-development through operations and closure—Sendero combines oilfield know-how with advanced measurement and reporting to help operators responsibly manage assets and strengthen long-term resilience. www.sendero-services.com

When I started working at Finboot almost two years ago, I couldn’t have imagined that blockchain could be used for anything beyond finance—let alone for something so impactful for the planet. Who would have thought this technology could become a powerful tool for delivering sustainability through the traceability of supply chains?

That’s exactly what this blog is about: showing how a platform like MARCO Track & Trace can make that vision a reality.

That’s where MARCO Track & Trace comes in: a blockchain-powered solution designed to help companies meet sustainability demands, build trust, and unlock entirely new revenue streams in the circular economy. More than just a reporting tool, MARCO Track & Trace is a comprehensive traceability platform that supports the transition to circular, low-carbon, and compliant value chains. What started as a solution for tracking and verifying product flows has matured into a full sustainability tool, helping leaders manage regulatory risks, improve transparency, and build consumer confidence. By streamlining tracking, reporting, and verification, it reduces uncertainty and empowers businesses to achieve their sustainability goals while staying ahead of regulations.

Which Are Marco Track & Trace’s Features?

Digital Product Passports: Transparency by Design

One of the most transformative features of MARCO Track & Trace is the Digital Product Passport (DPP). Think of it as a digital twin for every product—carrying with it all the essential information about sustainability, compliance, and performance throughout its lifecycle.

From raw material sourcing to the final delivery, the DPP captures:

Verified sustainability data like carbon footprint, renewable content, and circularity status.

Regulatory records and compliance documentation.

Immutable, blockchain-verified proof of every step in the supply chain.

As governments—particularly in the EU—move toward making DPPs mandatory for sectors like batteries, electronics, and textiles, MARCO T&T is already a step ahead; businesses can easily generate and manage multiple passports across batches and orders, share them automatically with stakeholders, and customize the content depending on the audience. This way, customers, suppliers, and internal teams get the information that truly matters to them—while ensuring every passport is fully compliant with ESPR requirements.

Or as Juan Carlos Perdomo, Product Manager at Moeve shared: “The product covers our needs in terms of traceability of our sustainable products portfolio supply chain. We're more than happy with the work methodology applied and the flexibility of the team towards our goals achievement.”

To make this even more intuitive, MARCO Track & Trace has launched the DPP Map, powered by MARCO AI—a graphical tool that shows supply chain flows in a clear, visual way. Amazing, right?

Mass Balance: Robust and Automated Inventory Management

Traceability in industries like biofuels, chemicals, or recycling is notoriously complex. Materials get mixed, reprocessed, and transformed. Keeping certified and non-certified materials strictly separate is often impractical. That’s where MARCO Track & Trace’s mass balance feature comes in.

It’s a smart bookkeeping system that ensures the volume of certified input always equals the certified output—no matter how much physical mixing happens along the way. This ensures that sustainability claims are supported by robust data, even if the certified content is not physically isolated.

Guaranteed integrity through prevention of double spending.

Ease of use for operators who don’t want to drown in complexity by easily sharing sustainability declarations with stakeholders.

As my colleague, Álvaro Llobet (Head of Product at Finboot) explains: “I believe we have one of the most robust inventory management systems available on the market today. Since we have all the data from the very beginning of a product’s life cycle, we can track inventory effortlessly and help you manage the product balance more efficiently and with far less complexity.”

Regulatory Compliance: Simplified and Integrated

For many companies, compliance feels like a never-ending battle—different regulations, endless paperwork, rising costs. MARCO Track & Trace turns that headache into a streamlined process.

By embedding compliance data directly into the Digital Product Passport, MARCO T&T helps companies meet the requirements of frameworks like EUDR, ESPR, RED III, and CSRD without the usual complexity.

That means:

Sustainability reports generated automatically, saving time and resources while ensuring compliance with environmental standards.

Compliance documents linked directly to product data.

Audits that go from weeks of prep work to just a few clicks.

Transparency throughout the supply chain by easily sharing sustainability declarations with stakeholders.

As Heinz-Günter Lux, Digital Strategist at Evonik, highlighted: “Finboot offers the most flexible and easy-to-implement solution for creating blockchain applications. It is extremely versatile and highly effective in applications like meeting data-driven regulatory requirements—even for users without a blockchain or IT background. The solution is intuitive to use and delivers excellent value for money.”

CO₂ Tracking & Calculation: From Cradle to Gate

One of the questions companies hear most today is simple: “What’s the carbon footprint of this product?”

With MARCO Track & Trace, emissions data isn’t buried in annual reports—it’s available at the product level, in real time, and fully auditable. The platform captures carbon and GHG emissions across the entire lifecycle: from raw material extraction to processing, manufacturing, and delivery.

Scope-based calculations aligned with the GHG Protocol and ISO standards.

Built-in frameworks for CSRD, CBAM, and CS3D compliance.

Carbon credit management with verified offset validation.

But MARCO Track & Trace goes beyond emissions tracking—it’s built to adapt. The platform has a flexible design that makes it easy to adjust processes, add new stages to the value chain, and introduce additional variables without any disruption. As Miguel Hernández, Chief of the Crude Oil and Heavy Compounds Lab of the Research Center of Repsol, says: “A highly professional team focused on proposing the best solution for each client, meeting objectives on time and in the right manner. Flexibility of the team and ability to integrate with other tools.”

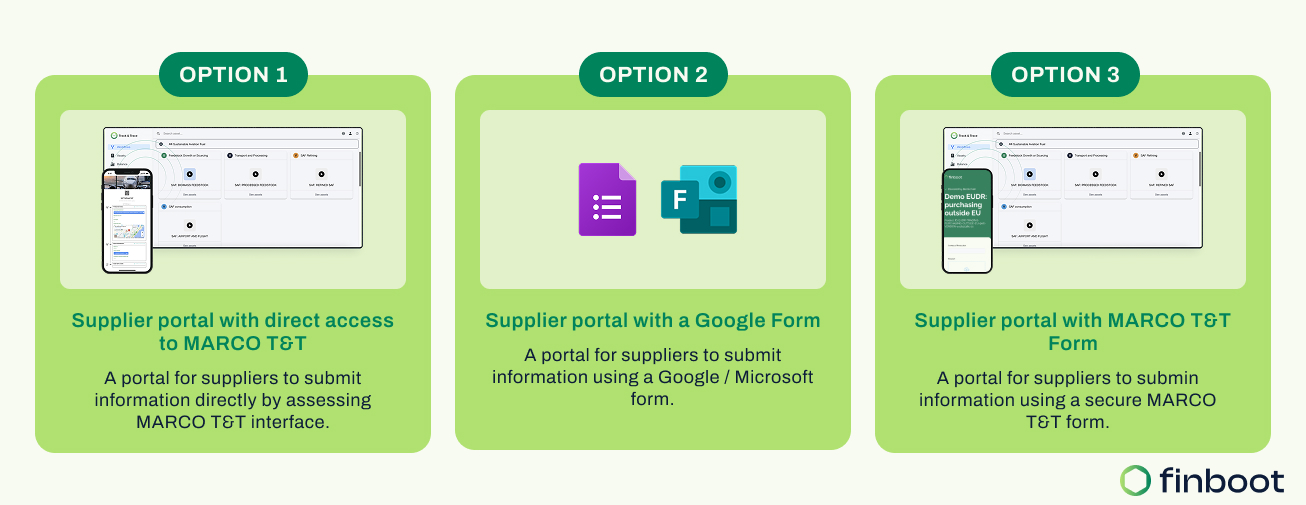

Supplier Portals: Collaboration Made Simple

Gathering sustainability data from suppliers is one of the toughest challenges businesses face. Different formats, inconsistent data, and endless follow-ups often make the process slow and error-prone.

MARCO Track & Trace solves this with supplier and customer portals—digital spaces where partners can easily share data, track performance, and collaborate on improvements, changing the way companies interact with their supply chain partners.

Through one of the three ways to access the portals —direct access to MARCO T&T, Google Form, or MARCO T&T Form— suppliers can:

Upload emissions and sustainability data with standardized templates.

Automate the collection and review of sustainability information

Get performance scores and benchmarking insights.

Receive risk alerts if their practices fall short.

Sustainability is no longer a side project—it’s the new foundation of competitiveness. Companies that fail to prove the origin, impact, and compliance of their products risk losing market access, investor confidence, and most importantly, customer trust. And trust isn’t just a feel-good metric; it directly drives business results. According to Adobe, customers demonstrate trust by buying more (71%), recommending the brand (61%), joining loyalty programs (41%), and posting positive reviews (40%). But trust is fragile—54% of customers stopped purchasing from a brand in 2020 because their trust was broken. Also, Gartner’s research shows top performers invest in digital technology twice as much as their peers.

That’s why first movers are already using MARCO Track & Trace to do more than “tick the box.” They’re cutting compliance costs, unlocking circular revenue streams, reducing carbon exposure, and building stronger relationships with customers. Leaders like Sabic, Moeve and Evonik demonstrate how scalable traceability delivers both regulatory confidence and business growth.

The opportunity is clear: transform your supply chain into a trusted, data-driven engine of growth. The risk is equally clear: get left behind as markets demand verifiable sustainability. The technology exists. The demand is rising. The leaders are already moving. The question is—will you move with them?

Digital traceability solution recognized for excellence in enabling verifiable sustainability data across global supply chains

LONDON/BARCELONA, July 25, 2025 — Finboot, a leading provider of digital traceability solutions for sustainable supply chain management, today announced its recognition as a High Performer in the prestigious G2 Summer 2025 Grid® Report for Sustainability Management Software. This independent recognition validates Finboot’s growing market impact in transforming regulatory compliance challenges into competitive advantages for global enterprises.

According to G2, the world’s largest and most trusted software marketplace, High Performer designation is reserved for solutions that achieve exceptional customer satisfaction scores while demonstrating significant market traction. This designation places Finboot among an elite group of sustainability management solutions delivering measurable value to customers, such as Osapiens, Assent and Workaviva. "Only about 10% of all vendors on G2 appear in our quarterly Market Reports,” said Sydney Sloan, CMO of G2. “Congratulations to Finboot for earning a coveted spot in our reports this season, a recognition powered by the authentic reviews of their customers.”

“This recognition from G2 represents a significant milestone in our mission to provide enterprise-grade digital solutions that drive both business value and sustainability objectives,” said Juan Miguel Perez Rosas, CEO and Co-founder at Finboot. “It’s particularly meaningful as it reflects direct feedback from verified customers who are successfully using our MARCO Track & Trace platform to address complex sustainability challenges.”

G2 reviews

Finboot’s MARCO Track & Trace solution distinguishes itself through its comprehensive approach to sustainability data management, offering features including Digital Product Passports, Mass Balance Bookkeeping, GHG Emissions Tracking, and specialized Regulatory Compliance Tools. The company’s recent launch of MARCO AI has further accelerated implementation timelines, with customers reporting a 98% reduction in configuration time for complex supply chain workflows.

The MARCO Track & Trace platform has demonstrated measurable impact across multiple industries, powering sustainability initiatives for global leaders including:

MOEVE; Energy/Chemical Manufacturing; 2023-present; Implemented digital traceability for sustainable linear alkylbenzene (NextLab) production, enabling transparent tracking of renewable materials via a mass balance approach. This resulted in fully auditable Digital Product Passports.

Repsol; Energy; 2018-present; Deployed verification system for renewable energy certificates and carbon credits, enabling transparent tracking and preventing double-counting across operations, with verified emission reductions.

SABIC; Chemical Manufacturing; 2021-present; Implemented supply chain traceability for circular polymers, creating verifiable documentation of circular material flows and enabling accurate calculation of the embedded carbon footprint for finished products.

Gestamp; Automotive Manufacturing; 2022-present; Established traceability for sustainable materials in automotive component manufacturing, enabling tier-1 supplier sustainability reporting and verification for OEM requirements.

Evonik: Development of a comprehensive digital ecosystem enabling EU Deforestation Regulation (EUDR) compliance across complex supply networks

“Finboot offers the most flexible and easy-to-implement solution for creating blockchain applications. It is extremely versatile and highly effective in applications like meeting data-driven regulatory requirements—even for users without a blockchain or IT background. The solution is intuitive to use and delivers excellent value for money.” noted one customer in a verified G2 review. “The Finboot team is highly competent, customer-oriented, responsive, and remarkably flexible in addressing individual client needs.”

The G2 Grid® represents the democratic voice of real software users rather than the subjective opinion of a single analyst. Products shown on the Grid® for Sustainability Management have received a minimum of 10 reviews/ratings in data gathered by May 27, 2025, with ratings based on customer satisfaction and market presence.

Sustainability management software has become increasingly critical as companies face growing regulatory pressures and stakeholder demands for transparent environmental performance. These solutions monitor resource use, carbon emissions, and other key environmental data points while supporting compliance with regulatory requirements.

For more information about Finboot’s MARCO Track & Trace platform and how it’s transforming sustainability management across global supply chains, visit www.finboot.com.

About Finboot

Finboot is transforming how companies manage sustainability data across complex supply chains. The company’s flagship MARCO Track & Trace platform leverages blockchain technology to create immutable, verifiable records of sustainability information, enabling businesses to meet regulatory requirements while creating competitive advantage through data-driven sustainability initiatives.

About G2

G2 is the world's largest and most trusted software marketplace. More than a million people annually — including employees at all Fortune 500 companies — use G2 to make smarter software decisions based on authentic peer reviews. Thousands of software and services companies of all sizes partner with G2 to build their reputation and grow their business — including Salesforce, HubSpot, Zoom, and Adobe. To learn more about where you go for software, visit www.g2.com and follow us on LinkedIn.

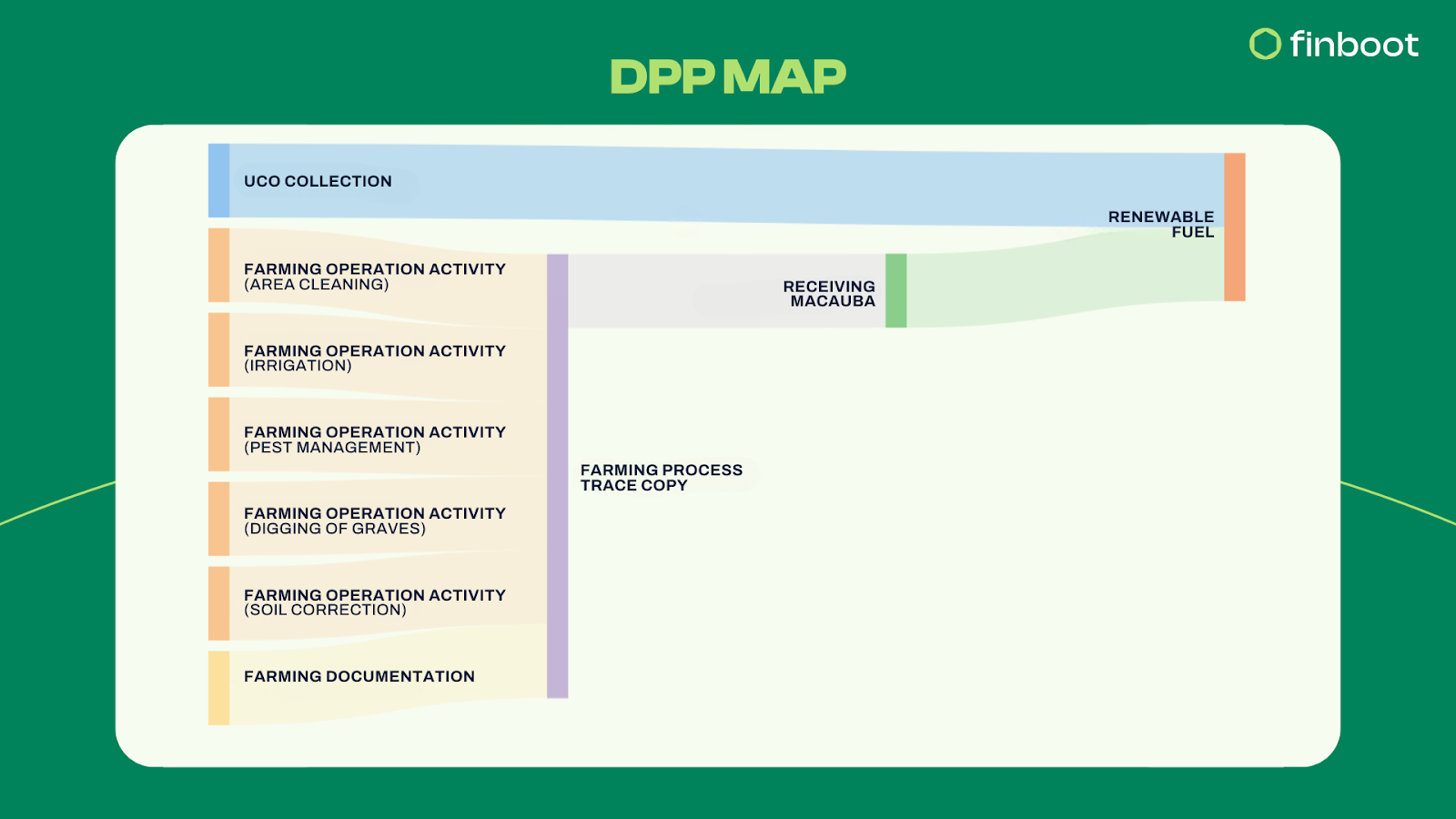

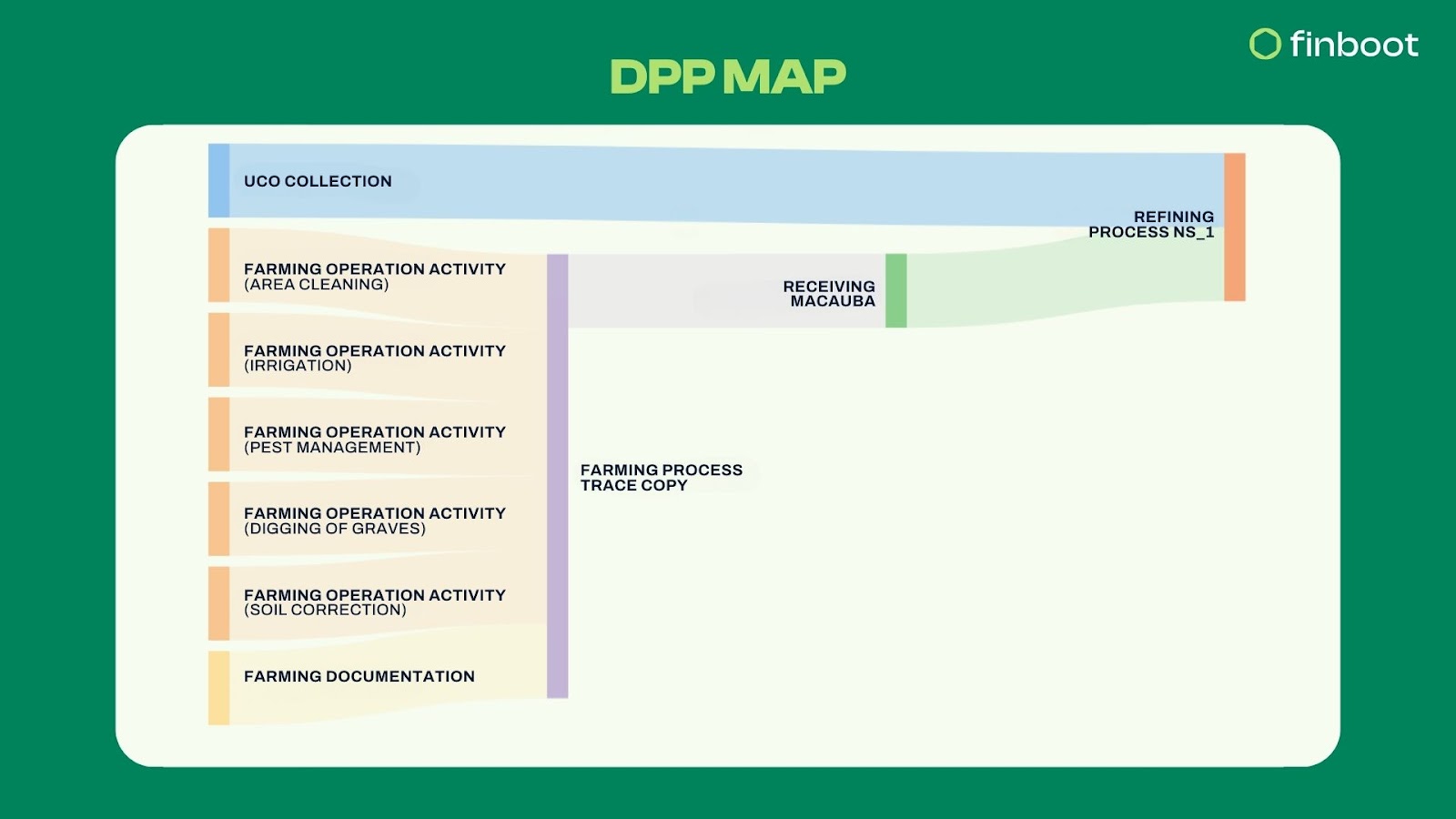

Digital Product Passports (DPPs) are the cornerstone of Europe’s circular economy. By capturing detailed information about a product’s lifecycle—from raw materials through to recycling—they promise to empower consumers, help businesses stay compliant, and accelerate sustainable innovation across industries. But the challenge has always been the same: how do we turn all this data into something that’s actually useful—something that’s clear, traceable, and easy to work with?

At Finboot, we’ve been working on that answer. Our latest feature—DPP Map powered by MARCO AI—takes what used to be a slow, manual process and makes it fast, intuitive, and scalable. It’s a big step forward for companies navigating the EU’s sustainability rules while staying competitive in an evolving market.

But the DPP isn’t just about ticking a regulatory box. It’s meant to support better design, longer product lifespans, smarter purchasing decisions, and more circular business models. It also makes it easier for authorities to verify compliance and for companies to track and share sustainability data.

Each passport will be connected to a product through something like a QR code or RFID tag, and the information must be easily accessible to everyone from manufacturers to customs officers and consumers.

The European Commission is already laying the groundwork, having launched a call for evidence to shape the rules for future DPP service providers. With the ESPR now in effect, the pressure is on to move from planning to action.

That’s exactly where Finboot’s DPP Map comes in.

From Manual Mapping to Instant Visuals: The Power of DPP Map

At Finboot, we’ve always worked closely with our customers to understand their supply chains. Typically, this involves in-depth discussions to uncover their needs, identify key assets and workflows, and then configure these processes within our MARCO Track & Trace platform. It’s a collaborative, human-driven approach that ensures traceability systems reflect real business operations.

But now, we’re taking that process one step further.

We’ve been building what is essentially a ChatGPT inside MARCO T&T—an intelligent assistant that automates the way we capture customer requirements and translates them into traceability workflows. Until now, creating a Digital Product Passport often meant long hours mapping processes, consolidating data, and configuring workflows. Simplifying this creation process was a strong request from our customers, and we’re delighted to launch DPP Map—a powerful, user-friendly graphical tool that complements the traditional data-heavy approach with a clear visual representation of the supply chain.

Now, users can:

Trace: Follow the complete lifecycle of materials and products with a Digital Product Passport that serves as a comprehensive, traceable record.

Access key details: Each DPP includes essential, regulation-specific documentation tied to a unique batch reference. Whether it’s hosted on a website, stored as a file, or delivered through another digital format, the information is structured and easy to access.

Visualize with DPP Map: Instead of digging through dense datasets, users get a clear, intuitive view of how components flow through each production stage—making supply chain insights easier to understand and act on.

Why AI Is the Missing Piece

Building DPPs involves understanding the unique context of every company: what regulations they face, what products they make, how data flows through their systems. This level of customization used to require close collaboration with each customer, lengthy onboarding, and manual configuration.

As we recently explained in a press release, Finboot has long been at the forefront of using technology to help companies understand, monitor, and build green supply chains. Now, to stay ahead of growing complexity and demand, we have integrated the power of GenAI into MARCO Track & Trace. These AI-driven innovations include the DPP Map that I’ve been explaining, and the AI Copilot.

To give a little context, with the AI copilot, users (using natural language input) can now say: “We’re an energy company sourcing oil from Costa Rica, and we need traceability across multiple workflows and regulation frameworks.” And MARCO AI will generate the digital supply chain infrastructure they need, from assets and workflows to checkpoints and attributes. It’s a true copilot—not just a prompt-and-reply assistant, but an integrated system builder trained on years of supply chain logic.

Privacy Without Compromise

Enterprise AI adoption often stalls on one key concern: data security. At Finboot, we understand this. That’s why our GenAI was designed to protect customer data at all times.