.svg)

Transparency Is Now a Capital Allocation Strategy

For more than a decade, transparency in heavy industries has been treated as an operational concern: a data challenge for sustainability teams or a compliance workflow to satisfy evolving reporting regimes. But that framing no longer matches the realities facing industrial leaders. As regulatory timelines accelerate and value chains become more exposed to disruption, transparency has quietly moved from the periphery of corporate agendas to the centre of boardroom strategy. In today’s environment, transparency is directly shaping how companies deploy capital, manage structural risk and evaluate pathways for growth.

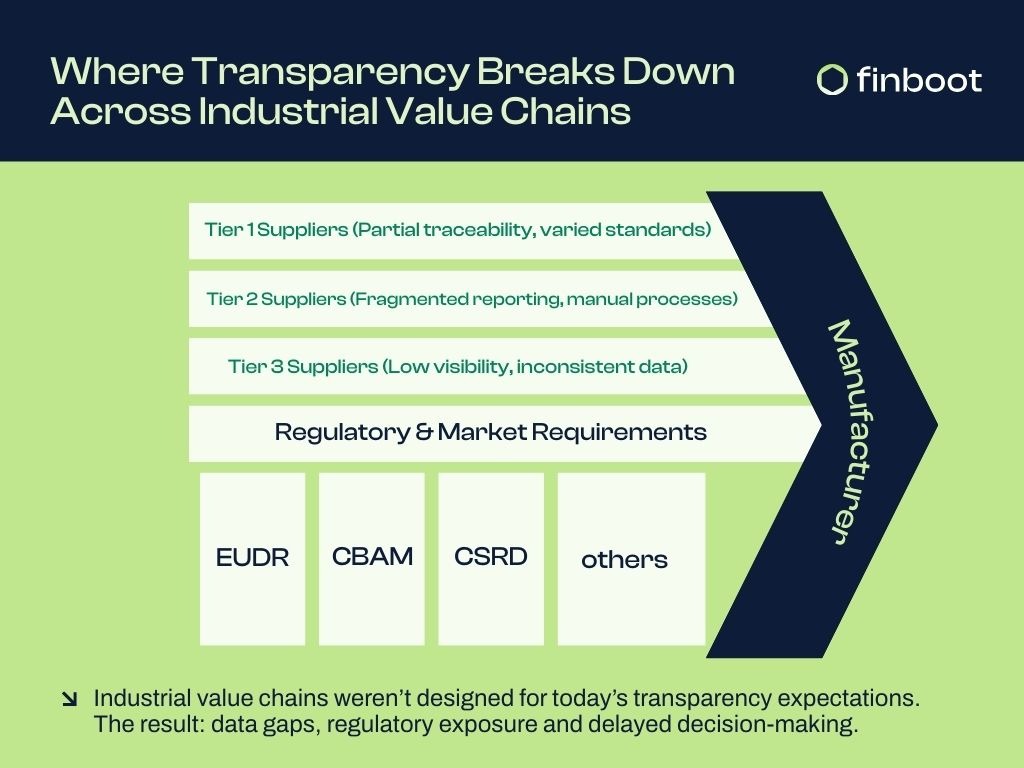

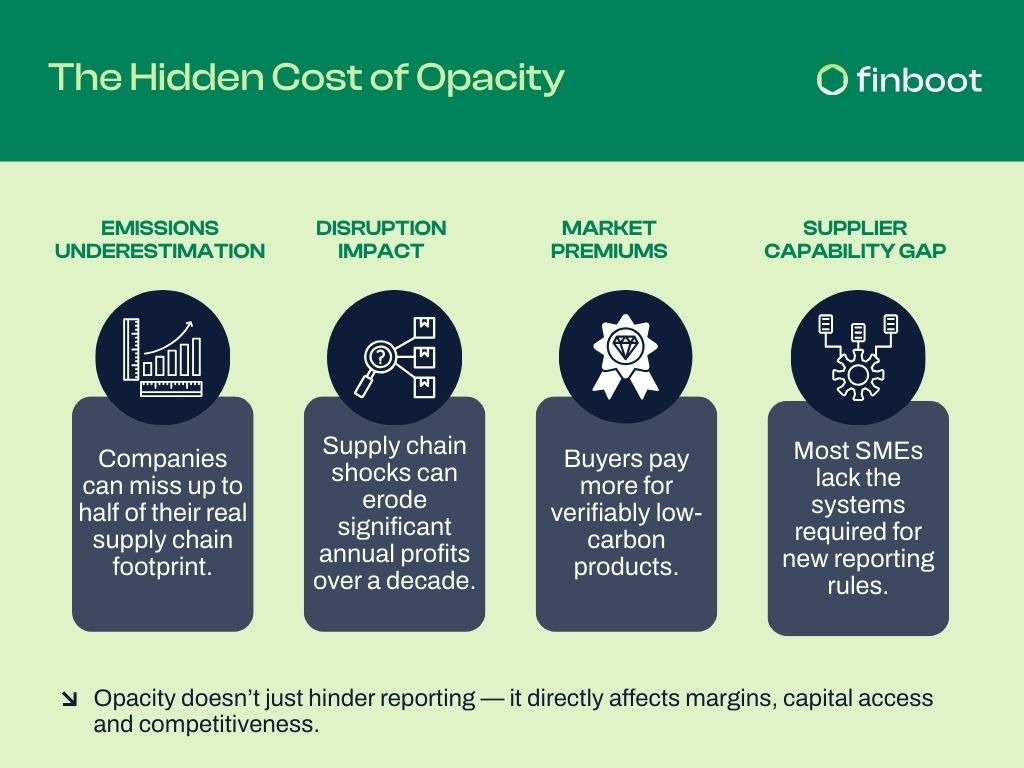

One reason for this shift is the increasing financial cost of opacity. According to CDP, companies with incomplete supply chain data underestimate their emissions by around 50% (CDP Supply Chain Report). This blind spot has material consequences. The European Union’s emerging regulatory frameworks—from the Corporate Sustainability Reporting Directive (CSRD) to the EU Deforestation Regulation (EUDR) and the Forced Labour Regulation (EU Forced Labour Regulation)—now link supply chain transparency directly to market access, financial exposure and credibility. Missing or unverifiable supplier information is already slowing investment decisions and undermining capex planning, particularly in sectors such as steel, chemicals and mining where margins are thin and asset replacement cycles are long.

The World Economic Forum estimates that supply chain disruption costs companies an average of 45% of one year’s EBITDA over a decade (WEF Global Risks Report). When opacity amplifies this volatility, the cost is strategic, not administrative.

Opacity also narrows a company’s ability to differentiate at a moment when markets increasingly reward verifiable sustainability performance. Research from McKinsey shows that B2B buyers are now willing to pay 5–20% premiums for products with demonstrably lower carbon intensity or traceable origins (McKinsey: The case for green products). Without credible transparency, companies are pushed into competing solely on price in sectors where price competition is already severe.

Yet the greatest structural bottleneck remains supplier engagement. Heavy-industry value chains depend on SME suppliers that often lack digital tools, standardised reporting frameworks and internal expertise. The OECD notes that more than 70% of SMEs feel unprepared to meet new sustainability reporting requirements—not due to unwillingliness but due to capability gaps (OECD Green & Digital Transformation of SMEs). This misalignment creates friction precisely where resilience is most needed. When transparency is positioned as a compliance burden, resistance is natural. But when it is positioned as a mechanism for suppliers to access new markets, secure longer-term contracts or qualify for sustainability-linked finance—an IFC priority area forecasted to exceed $1 trillion annually by 2030 (IFC Sustainability-Linked Finance Market)—the dynamic fundamentally shifts.

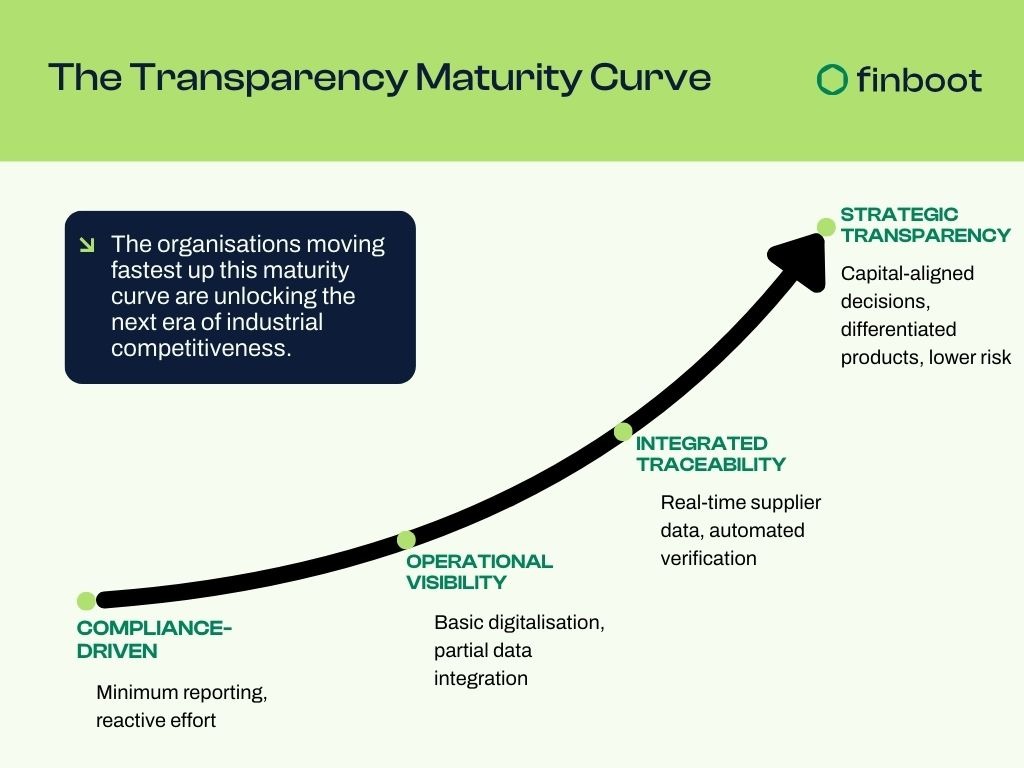

For executive teams, the return on transparency is therefore multidimensional. It reduces exposure by making regulatory and operational risks visible earlier, allowing leadership to avoid costly surprises. It improves capital efficiency by strengthening eligibility for sustainability-linked loans and reducing risk premiums associated with opaque value chains. It enhances competitiveness by enabling credible differentiation in markets that increasingly reward verifiable performance. And perhaps most importantly, it restores strategic optionality—the ability to pivot sourcing models, enter new markets, redesign product portfolios or allocate capital with confidence because the underlying data is trustworthy.

This is also why digital traceability is emerging not as another tool but as infrastructure. Just as ERPs became foundational to finance and logistics platforms became essential to global operations, traceability systems are becoming the backbone of sustainability, compliance and supply chain orchestration. They connect fragmented data flows across suppliers, transform manual reporting into real-time verification and enable organisations to turn regulatory pressure into strategic clarity.

Across industries, we are already seeing how organisations that treat digital transparency as infrastructure unlock resilience and measurable value. In sustainable chemicals, for example, Moeve has implemented end-to-end traceability across its palm-oil supply chain to support the launch of its first sustainable LAB, automating mass balance processes, improving data accuracy and strengthening customer trust through transparent product passports. In the circular materials sector, SABIC has achieved batch-level traceability from waste feedstock to packaging, enhancing the credibility of chemical recycling, reducing audit burdens and reinforcing accountability with partners as recycled content scales. In specialty chemicals, Evonik has adopted a fully digital, auditable approach to compliance with deforestation-free sourcing requirements, automating supplier documentation and geolocation risk checks to ensure that palm-oil-based ingredients meet strict regulatory thresholds. And in the energy industry, the partnership between Finboot and Sendero demonstrates how synchronising field-verified methane measurements with blockchain-enabled traceability creates an end-to-end auditable workflow that not only meets methane reporting standards but also unlocks premium market opportunities and carbon-credit revenues.

Together, these examples reveal a structural pattern: when transparency becomes embedded as core infrastructure, organisations move beyond compliance to shape competitive advantage. They gain the ability to operate with speed, certainty and credibility in markets defined by constraint. Ultimately, transparency is no longer a technical exercise — it is a leadership decision. And the companies willing to act on that decision today will be the ones defining industrial competitiveness tomorrow.

Ultimately, transparency is no longer a technical exercise—it is a leadership choice. And the companies willing to act on that choice today will be the ones defining what competitiveness looks like tomorrow.

.svg)

.svg)

.svg)